# 33 | Olympus (II), a Coming-of-Age Story

Ode to the Year Without a Summer

We owe much to 1816, the year without a summer. To the fear and boredom brought by the corrosive rains and ash clouds portrayed by Joseph Turner while looming over the seas and the Thames. Destruction and creation will probably for ever remain inexorably bound. Hard times test characters, relationships, communities, and of course business endeavours. It doesn't take much to have faith when the world is shouting at you to keep enjoying the ride. It is from hardship, however, that the best in us can emerge, when in the night’s darkest hour a solution needs to be found in order to avoid oblivion.

Four months have passed since I wrote a first piece on the Devourer of Planets. Four not uneventful months. That piece made me several enemies and as many friends. Because that’s what Olympus does: it splits families and ruins your Christmas dinners. Olympus is the crypto version of Donald Trump, or of Great Thunberg, it depends on which side of the dinner table you are sitting. Ultimately they are just two blondes. Yes, I have touched upon Olympus in several occasions but too often partially and imperfectly. This was unfair and I apologise.

So here we go. Olympus chapter II, redux. This one’s for the warriors.

The Calm After the Storm

DR #33 is not supposed to go back to the detailed mechanics behind Olympus’ original bonding-staking-inflating model - for that I’d suggest to navigate other articles from the homepage. As part of my first article on Olympus, back in October, rather than framing pros and cons of the $OHM model as a good management consultant would have done I took the sneaky shortcut of the mathematician (a smart bunch) and went for a proof of contradiction - or reductio ad impossibile as my people would have said a few thousand years ago. In other words, I asked myself whether Olympus (and its offspring) could have kept expanding for ever, swallowing one gigantic pool of liquidity after another. Would it have been plausible for all universal liquidity to remain trapped beyond Olympus’ event horizon without causing destructive effects in the fabric of the DAO or the whole DeFi ecosystem? Probably not, I had argued. At some point the centrifugal forces, i.e. the pressure for an accretive use of the assets attracted within the event horizon, would have outpaced the centripetal ones, and Olympus would have started to release back energy abruptly until reaching equilibrium. I don’t like to say it, but I was right.

Yesterday <> Today

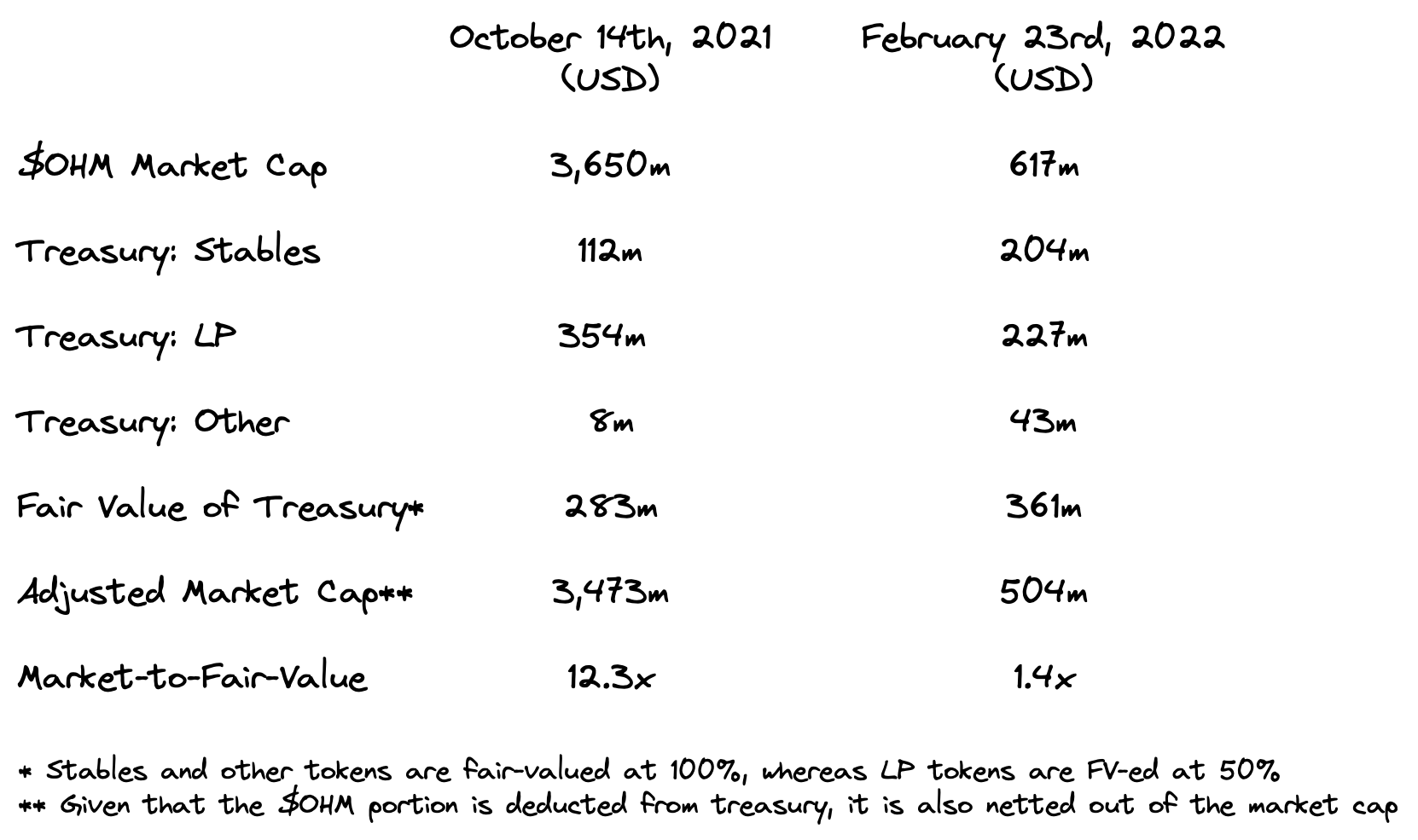

14th of October ‘21 → By that time Olympus had amassed c. USD 460m of assets in its treasury (at market value) consisting almost entirely of risk-free stables (c. 21% - $DAI, $FRAX, $LUSD) and LP tokens - c. 77%. Liquidity was obviously provided for all the $OHM vs. stable pairs so there is some recursiveness going on in the market valuation. If we take 50% of the LP position (i.e. assuming no arb and discounting the value of Olympus’ own tokens from treasury - and market cap) and 100% of the rest (risk-free stables and other tokens) we can estimate a fair valuation of treasury of c. USD 285m, and therefore a Market-to-Fair-Value multiple of c. 12.3x - see the table below. The market, in other words, was expecting Olympus to be able to generate enough economic value for its investors to massively overcompensate those investors’ cost of capital. I am not adventuring here in estimating Ohmies’ cost of capital but I assume it is not negligible, and that means that the expected future economic returns of the $OHM token were incredibly high-er. The treasury composition gives us a hint on Olympus’ ability to generate such superior profitability; i.e. it could have done so only by providing liquidity to the $OHM market and by managing somehow its stable reserves. With the returns on the liquidity provided ranging around c. 10-15% (back-of-the-envelop calculation with c. USD 38 of cumulative LP fees printed so far) that means the market was assigning an incredibly high premium (again, we are assuming market rationality) to the protocol’s ability to use the risk-free stables productively. Some Ohmies liked to call this premium currency/ seignorage premium, based on the ability of Olympus to become a new-generation reserve currency of the world. For me, math didn’t add up.

23rd of February ‘22 → A lot has happened in the following four months. Treasury went all the way up to USD 850-900m (again, at market value) and then back at c. USD 475m. Its composition has changed thought, with risk-free stables now representing c. 43% of total - obviously also due to $OHM price collapse, liquidity c. 48%, and the rest composed by some $wETH and $CVX. It actually makes a lot of sense for Olympus to start playing a part in the Curve wars, but more on this later. Giving a credit of 50% to the LP positions we reach a fair value estimate of c. USD 360m, now vs. an adjusted market capitalisation of c. USD 500m for $OHM. The Market-to-Fair-Value multiple, in other words, went from 12.3x down to 1.4x. Return on capital is still assumed to be higher than its cost (with the multiple sitting comfortably above 1x) but we are now at more reasonable levels and we can finally engage in a meaningful financial discussion rather than arguing about thin air.

I am not duplicating charts that already exist somewhere else. Once more, Dune is our best friend.

A similar (or worse) fate has met the most relevant forks of Olympus, including Klima and WonderLand, and many are giving the Big Daddy for dead. I am, on the contrary, starting to get interested. Many things have changed within the Olympus community, and at the valuation levels described above we can actually start having a rational debate about value, and price.

The Coming of Monetary Policy

While most Ohmies were defending orthodoxy at all costs, or simply abandoning the project, some core team members were learning. On the 11th of February Zeus issued a white paper called Exploring a Bond-Centric Future, advocating for radical innovation. The release of the paper might well be the most important milestone following Olympus’ birth.

In the paper the authors recognised that while the original construct, aimed at an aggressive targeted treasury growth to be obtained through extreme staking rewards, had allowed (also thanks to strong macroeconomic tailwinds) the protocol to bootstrap from zero to hundreds of millions in a very short period of time, it also generated destructive levels of volatility. The staking model, reflected the authors, had the benefit of protecting holders from dilution and stabilising liquidity in expansionary market conditions. Treasury, however, was constrained by mono-directional rails (assets could only be attracted and not given back) and by a passive stance to market making for the native token. The model didn’t equip the protocol with the required levers to counteract liquidity crunching. We had argued this all along and it felt good to read it in clear letters.

The paper continued by suggesting a new paradigm now centred around a new protocol primitive: internal bonding.

External bonds → Olympus v1 had considered only so-called external bonds. Those bonds acted as an incentive for new entrants to provide eligible assets to treasury in exchange for a discounted amount of native tokens. Using TradFi jargon, Olympus was embarking in a continuous (although parametrical) token issuance denominated in selected stables. As for most issuances, the purchase of newly minted tokens came at a discount - and that discount at the cost of diluting existing shareholders. Staked $OHM holders had always the ability to unstake $OHM → sell it in the open market → bond it for more tokens → and stake those again, but while doing so had to digest the bond’s illiquidity in exchange.

With staking rewards surpassing bonding benefits, and a constructive pressure on price, the arb opportunities weren’t many. This guaranteed a sustained flow of fresh liquidity towards the protocol and also the fact that the bonding discount had to be sustained only once or thereabout by existing token holders. The retrenching of liquidity and consequent selling pressure changed everything. Now staked holders had indeed the incentive to sell to either go away or circle back via bonding. This initiated a seller’s market and amplified the dilution effect for staked holders, exacerbating selling pressure further. Surprise surprise, the (3, 3) was just BS.

Internal bonds → In order to counteract those forces the authors of the paper proposed the introduction of internal bonds, i.e. instruments that would provide treasury with the ability to buy-back the native token (at a slight premium vs. market price) in exchange for backing assets. The ability to buy back would act as a valve, to release pressure and avoid the death spiral. Based on Olympus documentation the protocol is now implementing a simplified version of those bonds, called inverse bonds, that has no vesting and would only be available when $OHM market price falls below the market value of the backing asset - we are extremely close these days. Zeus’ original proposal, however, was more sophisticated and way more ambitious.

In its proposed form, internal bonds would not have immediate effect. Instead they would have a maturity date, or actually a fixed expiration - rather than fixed maturity, making them ERC20 eligible and therefore more easily tradable in secondary markets. For each $OHM deposited the bond would give the depositor the ability to claim x $OHM at y date, where x is assumed to be greater than 1.

More importantly, the base staking reward would be reduced in concert with the issuance of those tokenised bonds. The implications of these nuances are huge: with termed maturity, contractual staking yield, and tradable form, traders could now spin a secondary market around real termed yields - something that hasn’t yet happened en masse anywhere in DeFi. In the past, participants’ engagement was limited by the incredibly high staking reward rate - it wasn’t rational for anybody to get involved in any activity that would have provided a nominal yield lower than the x,000% reward. By reducing base staking yields and, in conjunction, introducing alternative sources of yield trading, Olympus could give birth to an expanding set of use cases within its own token market. Said differently, such a combination would reduce the protocol’s cost of capital (making its growth more sustainable) while at the same time expanding the protocol’s use cases and therefore sources of revenues.

Segmentation → A bond-centric approach (and lower staking yields) would also allow the protocol to strategically select (parametrically) the way $OHM tokens are deployed. Olympus, taking the example described in the whitepaper, could decide to allocate a 10m $OHM supply as following:

1m $OHM paired against other assets in protocol-owned LP

1m $OHM staked as $sOHM yielding 100% APY

1m $OHM deployed in various opportunities earning > 100%

5m $OHM locked into bonds across various expiration dates

2m $OHM paired with bond tokens to facilitate their secondary market

The effects of the segmentation are multiple:

A base rate of return is set through the staking yield - ideally at more sustainable levels

There is now room for alternative uses of capital as long as they yield more than the staking rate - in real terms, improving diversification and sustainability further

Liquidity is still guaranteed but now spread across multiple maturities - reducing immediate selling pressure in volatile conditions

The creation of a term structure is facilitated via the fixed-expiration bond market, expanding Olympus’ use cases into a new area

The new mental model introduces a huge amount of complexity, and therefore execution risk. In the short term liquidity would be further segmented and it is unclear what effect this would have on an already-strained token price. In addition, market inefficiencies could make the whole structure unfeasible, pushing more Ohmies to abandon the ship. Considering this, the staged approach of adopting first an extremely simplified version of those bonds, i.e. the inverse bonds, seems appropriate.

The EconOHMy

That doesn’t mean it isn’t worth trying. In its v1, beyond the memes and the wen Lambos, Olympus had attracted practitioners’ attention by internalising the market making of its own token and then by productising such approach for other protocols - via Olympus Pro. Olympus, using Chitra’s words (h/t Eric) was the first protocol to combine all aspects of liquidity provisioning previously tested (buy, lease, rent) with the aim of creating a low-vol reserve asset that could be used in treasuries. Chitra’s mathematical formalisation of Olympus is an absolute masterpiece, one that sucks the will to keep writing out of my soul so hard I am tempted to go back suggesting new coloured pie charts for M&A pitch decks.

Although fascinating, market making internalisation was a small business (revenue-wise) and an incomplete stabilisation mechanism. Creating an environment that had the sole purpose of guaranteeing its own liquidity seemed recursive, but we now can see how it could have been the seed of a much more ambitious project. Whether the community had this in mind from the start is not for us to say, but it isn’t relevant. The so-called Web3 paradigm is giving investors the ability to observe in real time the evolution of a start-up like Olympus, and it is unsurprising that what we are seeing is extremely messy. Illiquidity and lack of transparency can be extremely beneficial for a project when things haven’t been sorted out yet - I wonder how pension funds would feel like if they could have immediate access to the mess happening in the young portfolio companies of the venture funds they invest in.

Like Zoom, or Peloton, Olympus found itself at the right place at the right time, but that isn't enough to guarantee its long term survival. The community, who has undoubtedly a lot at stake, is now pivoting.

On the 12th of January Olympus published its 1-year manifesto to create a decentralised, censorship resistant reserve currency for the emerging Web3 ecosystem. Frankly, I still do not understand why they keep insisting on the currency terminology. Why not opting for a decentralised, censorship resistant financial services platform for the emerging Web 3 ecosystem? At the end, that’s what it is.

Simplifying the chart above, we can summarise the direction Olympus is moving towards as follows:

Maintain $OHM purchasing power: the current token emission rate is unsustainable, and it will be reduced - the effect should be an improvement of the investors (and community) base

Increase trust in $OHM’s resilience: with $OHM finding its place in more and more DAO treasuries, and with a better and more transparent on-chain governance mechanism, Olympus could improve market perception - something crucial for a wannabe reserve asset

Improve the (targeted) liquidity profile of $OHM: a good reserve asset must be fungible and liquid, but not disorderly so - Olympus will try to deepen token liquidity across DEXs and CEXs, facilitating the creation of trading pairs and incubating protocols that build on $OHM

Expand the treasury’s revenue sources: ultimately, the protocol’s net assets will need to generate returns that are at least as high as its base reward rate - Olympus wants to do this by bootstrapping more use cases (rates trading is a clear example) and incubating a growing ecosystem that builds on its platform

Said differently, Olympus is improving its internal mechanics while doubling down on cooperation. Frax, Klima, Redacted, Lobis, Rome, Alchemix, Dopex, Inverse, Tokemak, Umami Finance, Debt, Vesta, Volt, Exodia, Liquity, Phantom, Prime, Spirit, Fiat, those are all examples of existing partners building on the Olympus construct. During the last months the creation of an Olympus Incubator was announced, as well as a Grants Program, and a charitable effort. Olympus Pro too is getting revamped. A lot is happening. Nevertheless, I argue it’s the math that matters most.

Olympus is somehow slowly and unsurely trying to implement what Terra has done in a more coordinated, but centralised, way. It is still too early to argue whether Olympus would be able to create, through $OHM, a monetary overlay onto Ethereum’s infrastructural layer. The project, if there is one, is incredibly ambitious and probably presents too many existential risks for any investor. It is, however, a project I want to believe in due to its organic nature and collaborative vibrance.

At 40% premium over the fair value of its net assets believing is reasonably priced. I will keep watching. Maybe one day there will be less (3, 3) flying around Twitter and I will feel less ethical aversion to buy. Ethics is the bogeyman of any rational investor.

unlimited inverse bonds I think would drain the treasury to zero? They say there's a limit to how much OHM they will buy so it will just defend the peg for a little while and then it'll be back to square one, no? Seems a lot like backing $18 billion UST with $1 billion of BTC.