# 38 | Anatomy of a Fund-Raising

Developing a Useful Checklist for Crypto Projects Looking for Money (Ok, Mainly Stablecoins)

When I sat to write # 37 | Capital Structures for Stablecoin Protocols: the Revenge of the Sith I couldn’t have imagined it would have attracted so much iinterest. The piece was fairly technical or at least accounting-ish, and dealt more with downside protection than upside excitement. This made me happy. Diligence and prudence aren’t the most popular concepts in the world we live in, and definitely not the most appropriate to turbocharge the popularity of anyone’s newsletter. Because ultimately newsletters are all about their writer’s popularity, isn’t it? No, it’s not.

As a writer I, too, am a human being, and as a human being I, too, have an ego. But I am trying to keep it outside of this safe space as much as I can. From its onset, I have wanted to keep DR as dry and useful as possible. There is enough pontificating out there, and it gets old pretty quickly. And so I decided to make this release useful for others more than myself, and structure it as a checklist. As some of you know I have the honour to be part of a team that is thinking about ways to raise funds for one of the largest and most influential projects in crypto — MakerDAO, and so I decided to describe my thinking process in a way that might be replicable and useful for others. This is the origin of post #38.

Disclaimer: although I am actively participating with others to make all this a reality, the ideas below represent solely my personal opinions.

The DIY Guide to a [Sound / Successful] Fund-Raising

I am the worst person to suggest the best strategy for a successful fund-raising in a web3 environment, and at least for a few of reasons. Reason #1 is that liquidity, in the age I come from, used to be a scarce resource. The burden was with the company to justify to prospective investors why they were on the road asking for money. The balance of power seems to have shifted in the crypto world, where paper valuations look often absurd, and investors are full of cash to deploy — to then go back and raise more. Reason #2 is that in the sector I used to mingle in, i.e. financial services, the question “what do you need this money for” wasn’t often the best one to ask. Financial institutions live surrounded by uncertainty and loyal to statistics, and learned on their skin that it’s good to have a buffer even if you don’t know what you need it for — yet. Reason #3 is that I am simply a bad marketer.

All things considered, however, I believed useful to formalise my thinking as a former banker and investor, and as MakerDAO’s community member, in the context of a potential very large fund-raising for the protocol. Based on what I have learned from successful DeFi projects I am not sure that the steps below should be followed in order, but I will still try to tackle those one by one for clarity.

Step 1 → Identify Fund Requirements

Ok, I exaggerated in saying it is difficult for projects that live surrounded by uncertainty to quantify funding requirements. Having a framework is crucial to steer the conversation, and to force actors in thinking logically about any funding request. The immense availability of funding we are observing in crypto often confuses founders, that believe in the mantra of just asking for as much as investors are ready to give. Nothing comes for free, and even if equity checks do not have a nominal interest rate attached to it, the teams should remind themselves that a crypto-dedicated VC might have a hurdle rate of return of 30-50% year-on-year. Compounding economic value at that rate is not an easy task for any project, and venture capitalists are a founder’s best friends until they are not.

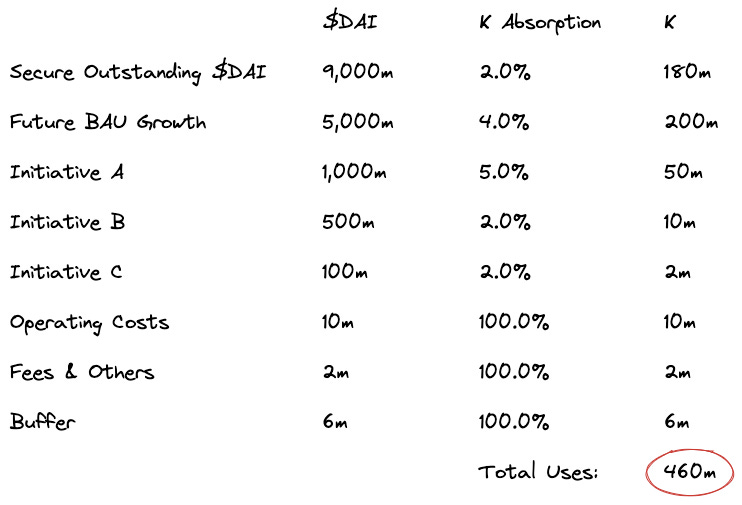

The framework below is a good one to stack funding needs of different nature one on top of the other — figures are obviously dummy.

Beware, liquidity is not capital → The table above solves for capital absorption rather than pure cash. This is the case because MakerDAO, as a sovereign stablecoin minter, can print liquidity in infinite amounts as long as the market keeps trusting the value of its own $DAI. For a bank (central, commercial, or crypto) liquidity is the product, not the raw material. The raw material is capital. A fund raising campaign should aim at gathering enough capital to provide a good buffer for all liquidity generation activities to keep trust strong even in the case of unexpected losses occurring — plus some operating expenses. Without enough buffer any unexpected loss might have catastrophic implications. The size of such buffer is up for discussion and is a risk management and capital markets question.

Capital sources are not created equal → As a reminder, in #37 we have argued for capital tiering and for the characteristics that qualify those various capital tiers.

Step two is figuring out what’s the best way to raise the identified capital gap. That’s where the fun is. We can learn from traditional institutions. As we have said before, capital sources can be ranked based on (i) permanence, (ii) ability to absorb losses, and (iii) remuneration optionality. Yes, straight equity/ token capital is by far the best source of capital we can aim for, but also the most expensive, and often it is unnecessary to fill the gap solely through a straight token issuance. Tokens are heavily dilutive, and in the case of DAOs they come with complex governance implications. Are there other options? For sure there are. Below are a few high-level ideas I would like to discuss with the DeFi community.

Those topics will be discussed later.

Step 2 → Investigate Investors’ Appetite

Raising funds is an art rather than a science. Especially for a protocol that has the ability to structure many different sources of funding. The post doesn’t argue about any specific secret sauce for fund raising, but tries to address the key questions that investors might ask, and that protocols should anticipate. We want to provide here a list of the key questions that a protocol should cover, and what the answers could look like for MakerDAO specifically.

Q1 → Are the interests of current equity/ token holders being taken into account?

(Governance) token holders rule, and token holders aren’t happy when the price of their tokens is depressed — try spending some time in MakerDAO’s forum these days. Growth strategies that require capital backing should generate long-term economic value that should be accretive for all token holders. However, even if we assume long-term capital accretion, token issuances might have a short-term signalling effect on tokens, have those been taken into consideration in sizing the equity raise? Token issuances have governance implications too, and those should be anticipated when roadshow-ing with existing and new investors. There is obviously an argument in favour of token issuance, as it has significant marketing benefits and it improves the liquidity of the token, but done wrongly a token issuance is a very bad move.

$MKR: MakerDAO’s current fully diluted valuation is c. $1.4b, a new token issuance in the range of $100-150m, or 10% of the float, could have limited negative implications both on valuation and governance rights if (i) the community understands the strategic and financial benefits, and (ii) there is a good mix of existing and new investors subscribing. But those are outside-in opinions, and ultimately is the voice of the market that matters.

Q2 → What are the available sources of capital investors have appetite for?

Venture capitalists are not the sole investors in the space. Up until the last ten year they were actually a very marginal bunch. The largest investors in the world have historically been banks, aka debt investors, and the thing shouldn’t be different in DeFi. Crypto-native VCs, traditional VCs and private equity players, credit funds — both traditional and crypto-native, other DAOs, and retail, should all be considered. Ultimately, every investor has appetite for a different source of capital: retail prefer a hand-off predictable yield, equity investors want control, banks want security, etc. We shouldn’t assume that checks from VCs are the only (or best) way forward. This brings us to Step 3, that will be discussed later on.

Q3 → Are incentives aligned across the capital stack?

A traditional bank (again, our closest comp) raises equity capital and the money received remains in the bank’s coffers and constitutes its Common Equity Tier 1 capital layer. Crypto banks are today a bit more complicated. Not necessarily (all) the funds raised through the issuance of tokens are in the protocol’s treasury in cash-like form. This is due to the various bootstrapping phases most OG protocols went through: e.g. private team → bootstrapping through a foundation → coin offerings → decentralisation. Today, some of the largest protocols hold a large amount of their own governance tokens as treasury assets — in corporate finance jargon the retention of own shares in treasury is in any shape or form similar to a capital reduction with the only difference being that a redistribution of those shares to the public doesn’t need to go thought the same governance approvals. This nuance is lost in the world of DAOs. Any outside investor putting capital at risk to offer protection to a project would expect the project itself to reach into its pockets first. Nevertheless, treasury management is a complex topic, one that has been already briefly discussed by DR — here.

$MKR: MakerDAO has benefited from a token transfer following the dissolution of the Maker Foundation. If I am looking at things correctly the protocol’s governance currently controls c. 82k $MKR tokens through MCD Pause Proxy contract — Etherscan, or c. $120m. This value is used today to incentivise the workforce, but doesn’t provide any protection to the protocol. As a reminder, the System Surplus is today only constituted by the earnings retained by the protocol through lending and liquidations at sits at c. $60m. How could the protocol monetise its treasury resources without negatively impacting token price is something that should be prioritised.

Q4 → Do returns justify the blended cost of capital sources?

In addressing investors, protocols should never forget to make a clear case that the additional potential returns from the initiatives would significantly outweigh the blended cost of all capital sources. That's where having a good view (although not scientific) on the uses of capital might help. Back to the table we were using before.

Most, but not all use cases, generate additional yields. Securing the outstanding liabilities with an extra cushion, for example, is not expected to generate additional returns, as well as paying for fees or other operating costs. In the example above, the initiatives unlocked by a fund raise would generate $113m in additional annual income — again numbers are dummy, and that represents a c. 25% return on capital. Looked differently, the capital raise would imply valuing additional income at a c. 4.1x Price to Earnings multiple - the inverse of the c. 25% earning yield. Is this enough to justify the capital raise? It is a question to ask capital providers. If crypto VC capital is the only source of funds, for example, it might mean that a 25% return is not enough to justify the VC internal hurdle rates. That’s where projects should get creative and use a combination of equity discounting, debt issuing, free grants, etc. to keep costs low and satisfy investors.

$MKR: Token prices and value creation is a very sensitive topic currently at MakerDAO. The $MKR governance token hasn’t had its best performance (both in USD and $ETH terms) over the last year. Putting additional weight on the token price via dilution or sell pressure is something that should be taken extremely carefully. Raising capital via an underpriced token further increases the effective breakeven yield that initiatives should generate.

Step 3 → Define Best Sources of Funds

Identifying or engineering the best funding structures is a protocol-specific effort. For most traditional corporates it is mainly a matter of sizing (some sort of) debt vs. equity. For most crypto projects things get more interesting with DAO-to-DAO solutions being explored — but that’s material for another one. For crypto stabelcoin protocols things get very interesting. Stablecoin issuers pay interests with their own product, and this means they have de facto infinitely expandable balance sheets. That is why we could get creative.

$MKR: Different from other stablecoin issuers (read Terra <> Anchor) Maker focuses on lending solutions (vaults) but not yet on yielding ones. Sure, the protocol could leverage external protocols like Porter Finance to structure a debt issuance, but wouldn’t that be a waste? As we have mentioned in #37 there are several potential benefits for a protocol like MakerDAO to develop native, $DAI-denominated, yield-bearing vaults for investors:

Total control and flexibility over contracts and parameters

Positive impact on $DAI demand (the flywheel effect)

Reduction of execution risk and (possibly) shipping times

Positive marketing and image impact for the protocol (the meme effect)

Tighter relationships with ultimate users and investors

A protocol-native debt solution could take many forms, but here is the way I am thinking about it — warning things are getting nerdy. The mental map below doesn’t want to be prescriptive but rather open the table for a conversation.

Going down the decision tree I reached three alternative models I’d like to emphasise here. Again, far from giving those exclusivity, but I guess it’s a good start: (A) $stDAI, (B) Internal Bonds, the (C) Insurance Pool. Below a bit more detail on each.

(A) $stDAI → $DAI are deposited in a staking contract in exchange for a parametrical (variable) staking yield. The $stDAI itself is an ERC-20 token that could be ideally tradable on AMMs like Curve. The staked token can be redeemed following an unstaking delay of 1-2 months in order to ensure availability of funds when needed — rather than reduce selling pressure on the token as it happens for staked $LUNA. $DAI staked will constitute an Insurance Buffer that will act as a second line of defence right after the System Surplus. In this construct, slashing risk wouldn’t derive from malevolent behaviour of the nodes but rather from extraordinary protocol losses that exceed the System Surplus — i.e. the first line of defense.

+ Tested avenue, flywheel effect for $DAI demand

- Size difficult to control, might require liquidity bootstrapping, makes planning difficult

Verdict: simple and tested but definitely not optimal for MakerDAO

(B) Internal Bonds → Maker could structure bonds that have a fixed term/ expiration (1-5 years) and pay a linear accruing interest rate, in exchange for a deposit of $DAI. Those bonds would remain tradable. There are several ways to structure those bonds, but $OHM’s internal bonding model has been well researched and has interesting implications — more on it here. Bonds would have a fixed expiration rather than a fixed maturity, making them ERC-20 eligible and more easily tradable in secondary markets. For each $DAI deposited the bond would give the depositor the ability to claim x $DAI at y date, where x is assumed to be greater than 1. Internal Bonds also act as a second line of defence behind the System Surplus.

+ Better control and visibility, flywheel effect, spinning a real yield market

- Refinancing at expiration not guaranteed, concept might be cumbersome

Verdict: fascinating and tested, probably simple enough, and providing good visibility

(C) Insurance Pool → $DAI can be staked in an insurance pool that yields a fixed rate of return. Those staked $DAI cannot be redeemed, ever, and remain perpetually staked à la Warren Buffet <> Goldman deal. They can, however, be called by the protocol — potentially with a pre-agreed premium. The idea is that the instrument is expensive for the protocol, and the protocol has an incentive to call it and give back the money to investors that therefore wouldn’t get stuck in for ever. At the same time the protocol has full control over its own buffer, a bit like equity. The staked $DAI could be traded out vs. $DAI as it happens for pre-merger Lido’s $stETH <> $ETH on Curve. The Insurance Pool also acts as a second line of defence behind the System Surplus.

+ Highest control, flywheel effect, elegant, perpetual yield might become a benchmark

- Might be too complex, unsure whether stakers would be comfortable with perpetuity

Verdict: elegant, with great visibility, but the perpetual nature might push some away

I have a preference for (B) and (C), but this is just food for thought and I am looking for the community’s feedback. Those solutions aren’t mutually exclusive, and could be tested at different times, or even stacked on top of each other in the capital structure — e.g. you first burn through the System Surplus then through the Insurance Pool then through Internal Bonds etc.

Step 4 → Minimise Cost of Funds

When the sources of funds have been defined, the following step will be sizing each, starting from the cheapest to the most expensive. This is the waterfall concept. Additional equity, ultimately, is our plug.

$MKR: In the case of MakerDAO, the cheapest source of funds should come from grants provided by side-chains and L2s to incentivise developers, as well as revenue rebates of any sort — read farming. The different types of debt discussed above should be number two in the pecking order and constitute the bulk of the capital raise — e.g. 100-200m. Treasury shares, or $MKR currently held by the protocol, should be next. Their usage as collateral for debt raising via other protocols like Porter, AAVE, or Compound would make them dilutive only in case the collateral is appropriated. If those $MKR-backed loans are raised conservatively, this should never happen. The issuance of new $MKR tokens should be the protocol’s last resort given the several (positive and negative implications) we touched upon in Step 2.

Step 5 → Execute & Iterate

Steps 1 → 4 is as far as a non-engineer like me can go, but it is definitely not far enough. Ultimately it is thanks to engineers and lawyers that those ideas can become a reality. All available solutions should be battle-tested with those who can make them real, and their feasibility should be checked at the most detailed level possible.

As we have learned times and times again, blockchain tech doesn’t forgive mistakes.

Thank you so much for this. Is there a way I can reach out to you? LinkedIn? or Twitter?

so, looking at your Q4 table, there would be no additional costs related to the new initiatives? No dev or legal expenses? Asking, because i wonder if there are costs we don't see because they're paid with tokens held in treasury.