# 47 | Tribes & Endgames: DAOs Stretching Themselves

Legendary Endeavours Can Have Dark Consequences

The Free State of Fiume emerged as a tiny independent city after a bunch of black-shirted nationalists seized the Adriatic port rallied by the poet and warrior Gabriele D’Annunzio. The short-lived Regency of Fiume was given a constitution, the Carta del Carnaro, never applied, describing a utopian blender of antiquated ethics and political modernism, where poems would be read at night in public squares and the order maintained by self-indulging groups of young males desperately looking for their place in the history books. D’Annunzio reigned as the sole enlightened dictator of Fiume for a good fifteen months, that is until the Italian navy bombed him out of town relegating the endeavour of Fiume to the obscurity of intellectualism but turbocharging, through folklore and rhetorics, the descent of Europe into the fascist insanity of the twentieth century.

Growing Pains

Roughly a month ago TIP-121 brought forward, formally, the intention of shutting down Tribe DAO, the governance arm of the stablecoin protocol called Fei. After the proposal, no matter the outcome, Fei Labs would have stepped away for good. As part of the proposal:

$FEI dollars could be redeemed for $DAI 1-to-1

Fuse hack victims could receive payment making most victims whole

$TRIBE holders could redeem the token for a pro rata share of remaining protocol-controlled assets

There are a ton of moving parts in what has been brought forward, and I do not want to focus this entire DR release on the matter. I have a good reason not to do it: the internal pains of Fei governance were my very personal Christmas 2021 obsession, back when Fei was merging itself with Rari Capital through a disordered and absolutely sub-standard process. I published a first piece on Fei <> Rari on the 9th of December, and a second one on the 30th. It was a pebble in the pond at the apex of Tomorrowland: i.e. nobody couldn’t care less. Even among insiders, notwithstanding the innumerable loose ends, the reaction to the proposal was overwhelmingly supportive, with 93% of the Rari community and 91% of Tribe’s voting in favour.

I wouldn’t have been so chilled as a stakeholder. The demonstrated lack of empathy for minority interest holders could have been a double-edged sword, ready to bite back. And it did. On June 12th Jai, Rari’s co-founder, slammed the door and left. On June 16th the Fuse hack repayment was denied on-chain, reversing a previous decision. On August 19th was the time of TIP-121 and the unwinding proposal. On September 9th the decision on the hack make-whole was revoted on and accepted—so much to scientific governance. In the middle flashed accusations of insider trading, equity holders favouritism, and other stuff.

It would have been better to challenge this type of behaviour early, rather than complaining at the turning of the table. I don’t have too much respect for the average quality of crypto journalism—saving rare exceptions I am happy to call friends, so I am giving us all another chance: let’s look at the signs early rather than shilling the good times and complaining when the prophets become the villains. The DeFi industry needs to step up and we all need to do our part.

MakerDAO: the Endgame Is Here

And so we get to MakerDAO, again, central in the DeFi ecosystem and in my life as researcher and practitioner—there is most certainly a correlation between the two. Less than two years after the launch of its attempted decentralisation process—MIP1 is dated May 2020, and after prolonged flirting and fencing, the protocol seems to have ultimately reached a crossroad. I won’t put it as a clash of narratives—narratives shift, but rather as the confrontation between two different set of motives. I will let the readers figure those out.

An alternative vision for the protocol has been floated for a long time by Rune, through very detailed, extremely articulated, unforgivingly frequent, excruciatingly long, posts and open calls. The shape of the so-called Endgame Plan (that ironically doesn’t ever seem to end) has been morphing with time, and it is difficult if not impossible to provide a comprehensive and coherent summary of it here. As a grey-haired-almost-forty researcher and investor, what made me skeptical was the evident unbalance between, on the one hand, the superficial description of the intricacies of wholesale finance—a world ruled by darkness, evil bankers, and unpredictable regulators, and on the other the painfully detailed explanation of the vaults, farms, value sinks, permissioned and permissionless operators, that the Plan would unleash. The latest version of the Plan (currently in its v3, here) would require a Tolkien-esque glossary of terms. I will leave you to it.

I am not the only one expressing concerns. LongForWisdom, former Facilitator of Maker governance, published a long and articulated op-ed on the potential issues of the plan. Given its focus on the nuances of political incentives I’d suggest anyone to read it.

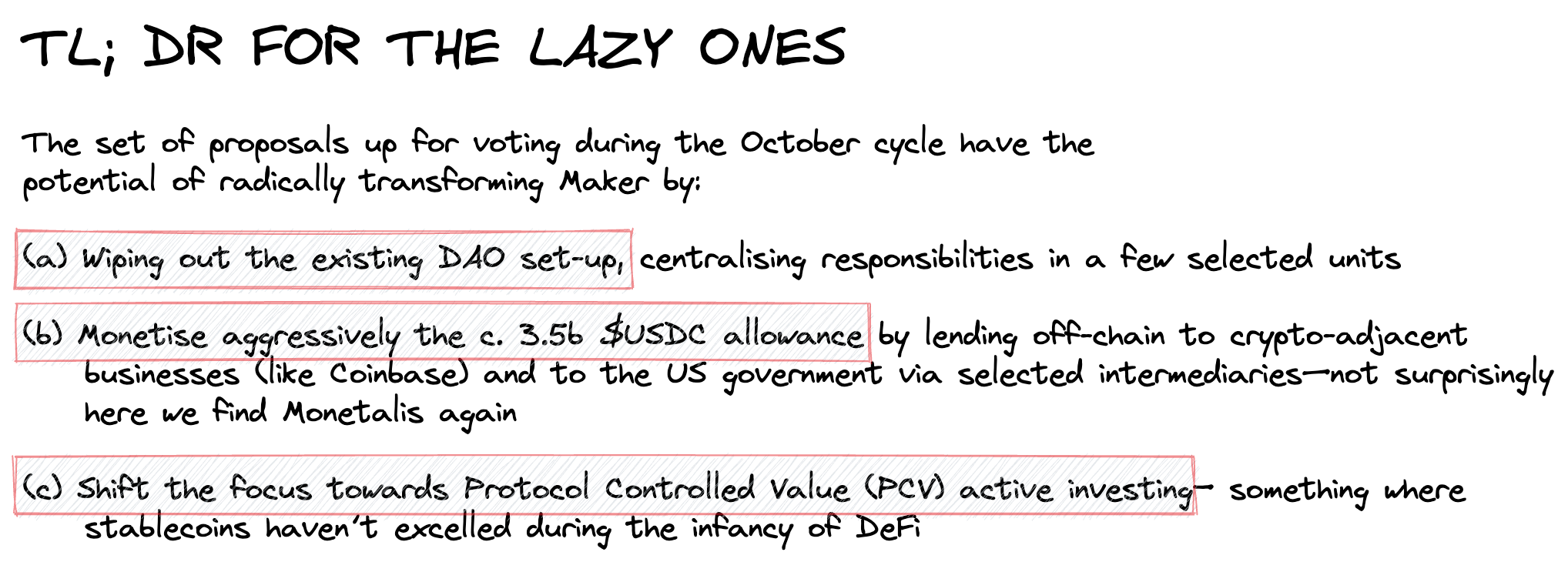

What’s up for voting today → Focusing our attention not on tomorrow or on the intricacies of the Endgame Plan, but rather on what’s actually up for voting today, reminds us that the upcoming voting cycle has arrived with a plethora of often-fundamental proposals, most of them authored (or at least grandfathered) by Rune—Maker’s founder. Their implications, separately and (especially) jointly, go very very deep. In the spirit of scientific governance analysis, I have decided to focus solely on what has been brought up for voting, as there is already enough meat to suggest what the new destination of the protocol could be. If you are a $MKR holder, I’d suggest you pay attention.

Let’s go straight to the meat: Maker would, de facto, move its focus away from smart contract-based CDP product deployment, towards a Fei-like PCV management model. I would strongly encourage large $MKR holders to deeply analyse the potential impact of those MIPs on their investment. Beyond that, the wider Endgame uncertainty looms:

The plan dilutes current $MKR holders through new emissions and multiple subDAO token farming schemes (most likely illegal securities offerings) that accrue to a select chosen few

It introduces several new regulatory risk vectors and attack surfaces that increase potential for large holders to face unlimited liability for criminal and civil actions

It risks acceleration toward a tipping point of fatal talent loss which will make execution of any roadmap impossible

One level deeper → We are nerds, here at DR, and we can’t stop at the surface. The many Endgame-related MIPs so far up for voting can be compiled as follows:

Governance wipeout: those changing fundamentally the way Maker’s governance works today

Endgame pre-launch: those preparing Maker to pivot towards the long-term goals advertised in the Endgame Plan—shift to a focus on PCV, implementation of the MetaDAO structure, clear marching towards a de-pegging plan grounded on opposition to regulators worldwide

Novel risk exposure: those introducing sizeable new risks in Maker’s balance sheet—in the form of huge off-chain investments, and development of an internal prop hedge fund

We have summarised those proposals in the table below—and you can find all the details on the Maker forum. All proposals are still in their Request For Comments phase, and their content can still change, also thanks to your comments.

In my opinion, the proposal to activate a Protocol Owned Vault Emulation (POVE) module deserves particular attention. It is a complex MIP with deep implications. Maker would start amassing $ETH and $ETH derivatives, programmatically, as part of the Surplus Buffer. Conceptually, the Surplus Buffer would go from being a cash-like cushion to protect against unexpected losses (in line with the concept of Common Equity Tier 1 capital of traditional banks—we had discussed it already here) to some sort of DAO-owned hedge fund with yield and volatility. The intention is then to reinvest in this way most of the yield generated by using the dollars in the PSM. The shift from being a permissionless set of smart contracts providing ability to leverage $ETH and $BTC to a Fei-like protocol-controlled fund that uses the $DAI stablecoin product to aggregate value is clear to me. More specifically, POVE would:

Identify a minimum required cash component for the Surplus Buffer—originally at a (negligible) 20m $DAI, beyond which $DAI in the Surplus Buffer will become fungible for the strategy

Maintain a list of whitelisted assets: initially $stETH, $ETHERDAI—not existing yet, $DAI, $LDO

Use extra $DAI to provide leverage for those whitelisted assets—although without a liquidation module to protect the Surplus Buffer against mark-to-market losses

Reinvest future profit flows into the strategy, including the yield coming from using the $USDC available in the PSM to purchase US treasury via few selected centralised operators—some with close relationships with the founder (e.g. Monetalis) and others under strict US regulatory scrutiny (e.g. Coinbase)

POVE launch would happen via immediate bootstrapping with 40m $DAI coming from the Surplus Buffer used to acquire $stETH, a possible augmentation via $LDO acquired by Rune—with a conversion of some treasury $MKR, de facto similar to a capital increase and dilution for you as $MKR holders.

The acquisition of 20m $LDO from Rune is another fascinating twist that rings all bells of insider dealing. Although Rune stated that his intentions are to help MakerDAO gain exposure to the success of Lido Finance, a protocol that he believes to be central to the long-term success of the Endgame Plan, I have strong concerns based on experience, since:

It is impossible to evaluate pricing appropriateness ex ante

It is impossible to second-guess the intentions for the swap—strategy, liquidity, tax, control, farming implications in the MetaDAO construct, etc., especially in the context of the broader Endgame Plan

The swap would exacerbate control issue further, reducing the control premium (and value) of the large stakes owned by $MKR whales

The regulatory (and fiscal) implications could be huge, and honestly unnecessary at this point

But is there an alternative possible for Maker? In my opinion, there is. Maker has proven to be an extremely successful, profitable, and scalable product within DeFi, and that’s where an alternative route could focus: simplifying the organisation and returning to healthy profitability—I am convinced that at least 30% of DAO costs could be cut without an impact on business and a proposal to move towards project-based budgeting has been already brought forward, progressively and conservatively improving the core product—e.g. via Layer 2 expansion, protocol-to-protocol liquidity, better risk management, and especially developing a constructive relationship with regulators worldwide.

Most importantly, this alternative future entails a more diverse democratic debate, requiring a way more involved participation of large governance token holders, directly or through a group of committed representatives that are endorsed by another $MKR majority. This is not only about the political infighting of a specific business or project, but rather about developing mature governance frameworks that move away from the myth and the legends. To me, it matters.