# 65 | Usual Money: a Valuation Framework

Choose Your Game. Master Your Game. Win, Lose, Own It

Disclaimer: as one of the co-founders of M^0, I have had extensive interactions with the Usual team, including collaborations, debates, and discussions on protocol mechanisms and yield distribution. While I strive to ensure that my research remains objective and rooted in first principles, I acknowledge the inherent conflict of interest in this context. It is up to you to decide if and how much weight to assign, or haircut to apply, to the analysis that follows.

The world isn’t the same anymore, as the old folks like to say. And I am old. Ah, I remember the days on Terra, and the chubby Korean playing Sauron. I remember the Olympus bonds and the (3,3). I remember the bloody Sushi vampire attack. I think back fondly to the gentle sunrises during the Curve Wars, when a soft breeze seemed to carry the illusion of quick riches, lifting our egos with the latent belief of being cleverer than those out there shovelling corporate shit for their pay checks. I dream of the dream of a green utopia, where a lucky few could sip biodynamic champagne in treehouses filled with Van Goghs, all courtesy of Klima’s black hole of hope. And who could forget the infighting between Rari and Fei, children against children like in the old days of the Montagues and the Capulets? It’s a strange nostalgia, bittersweet and sharp. But one thing’s for sure: it feels good to be back.

Far too much has been written about Usual Money, and yet, far too much about narrative and not nearly enough about substance. The discourse has been dominated by accusations (corporate treason, misbehaviour, technical rug-pulls, and misleading information) while rigorous, incentive-oriented, first-principles analysis of protocol mechanics, yield dynamics, and (most intriguingly) implied pricing has been sorely lacking. True to Dirt Roads’ tradition, I’ve donned the old robe and gone digging. So, here it is: a comprehensive, insightful value map to help you understand (and, hopefully only after that, interact with) Usual Money. If you’re deploying significant capital, and especially if you’re layering leverage on top of it, you owe it to yourself to know exactly what you’re doing. Follow the incentives, map the mechanics, and extrapolate carefully.

The Usual Investor: a Book of Practical Counsel

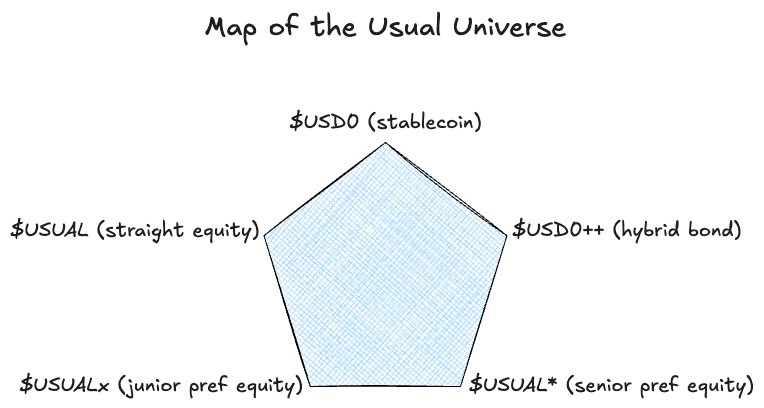

Usual’s on-chain capital structure is intricate, making any attempt to analyse it without a clear and coherent mental model both futile and counterproductive. To address this, I propose a framework that I describe in detail below.

So-what → The most crucial starting point is understanding what Usual is—or, more precisely, how Usual creates value. At its core, Usual aims to vampire-attack the liquidity currently parked on the balance sheets of stablecoin issuers and redirect its yield to a new set of stakeholders. How this yield is distributed among stakeholders is a secondary question, one we will inevitably address further down the line. As of today, this is the sole stated ambition of the project.

As we’ve discussed here many times, stablecoins are fundamentally scope economy products, requiring considerable counter-pressure to overcome the holding inertia and trigger a switch. The lack of adoption of basic yield-bearing or yield-distributing alternatives has demonstrated how the underlying 4-5% yield per se is insufficient to justify a migration to new entrants, and the attempt to solve the cold-start conundrum is at the centre of Usual’s value proposition.

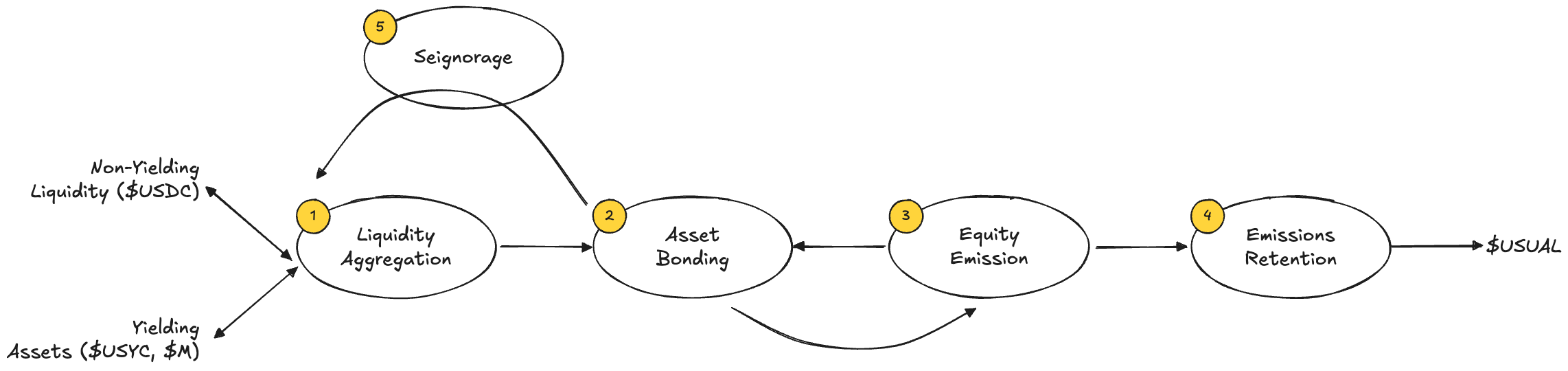

So-how → Usual intends to achieve this through a set of intermediate steps I describe below:

Liquidity aggregation: convince $USDC holders to deposit their liquidity in 1:1 exchange for $USD0—minted against tokenised risk-free proxies $USYC and $M

Asset bonding: lock $USD0 holders for the long term (4 years) via an on-chain bond called $USD0++ which holds some level of discretion

Equity emission: compensate $USD0++ holders for the foregone time value of money (i.e. illiquidity) through protocol equity issuance via $USUAL

Emissions retention: implement structuring mechanisms to ensure long-term value accretion (via $USUALx) and optimise residual yield for $USUAL*

Seignorage: reduce $USD0++ liability costs via utility and seignorage, thus increasing earnings retained by the rest of the capital stack

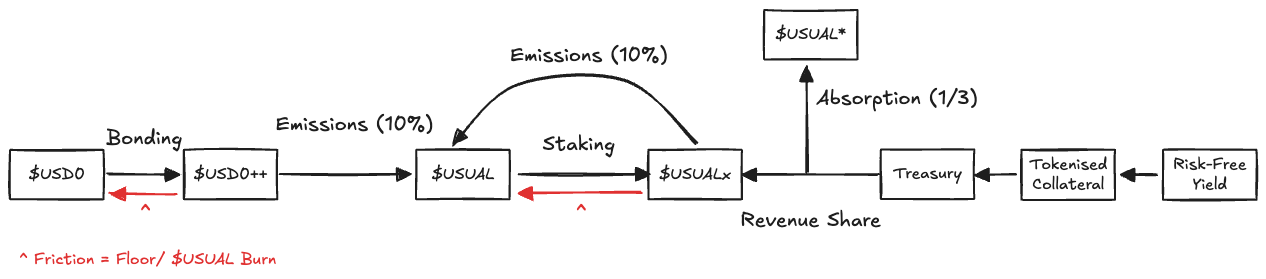

Below is a graphical representation of these phases. The remainder of the analysis will delve into each one, examining the mechanisms Usual has chosen and their high-level impacts on value transmission. Assuming that, in the early stages of the project, the sole incentive for interaction will stem from the pricing of $USUAL tokens—and not by $USD0 utility, the analysis will also attempt to derive the implied, probability-adjusted, value pricing as suggested by any rational investor.

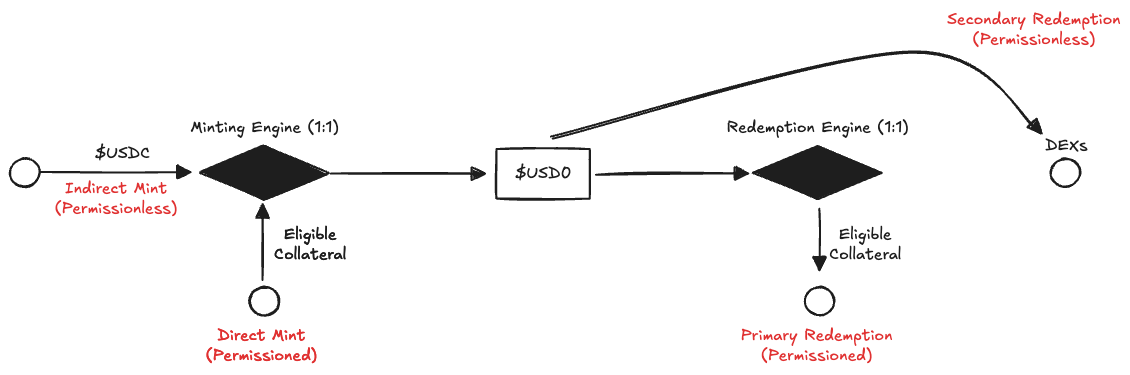

Phase 1: Liquidity Aggregation

As with many similar cases, Usual’s ultimate ambition is to persuade holders of $USDC (a non-yielding, junior, commingled US bank liability) to provide their liquidity to the protocol in exchange for something else. This liquidity would then be invested in on-chain, risk-free proxies, in exchange for a 1:1 mint of $USD0. Whether this occurs indirectly (via permissionless provision of $USDC) or directly (by supplying eligible collateral for primary $USD0 generation) is irrelevant. In this first step, the protocol facilitates the 1:1 minting process and retains 100% of the underlying yield generated by the tokenised asset proxies. Conversely, $USD0 can be redeemed 1:1 at any time for units of the underlying collateral or traded on DEXs for $USDC. Curve’s (incentivised with up to 2.5% of $USUAL token supply) $USD0/$USDC pool has currently c. $77m and allows swaps at par.

At present, the protocol’s TVL, amounting to more than $1.5b, is predominantly composed of Hashnote’s $USYC. Additionally, $UsualM—a bespoke extension of M^0’s $M token—has recently been integrated, contributing $50m to the total TVL. The asset yield absorbed is therefore a blend of Hashnote’s 3.1% and M^0’s 4.8%—soon down to 4.15%. The difference in yielding between those two assets is connected to radical structural differences that I cannot discuss here due to my blatant conflict of interest as CEO and co-founder of the M^0 project.

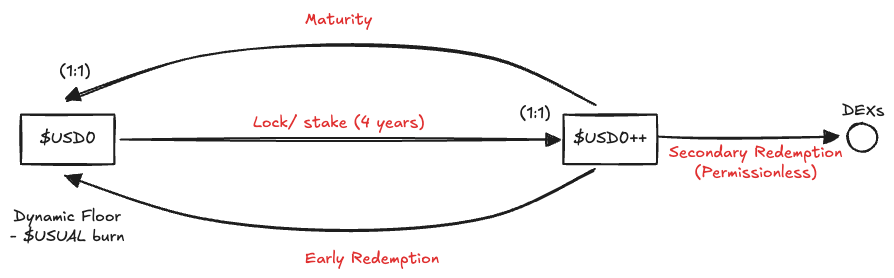

Phase 2: Asset Bonding

Since $USD0 functions as a non-yielding wrapper with currently limited standalone utility, its holders are incentivised to lock their assets for a predetermined 4-year period by minting $USD0++. This token, also minted on a 1:1 basis, is a zero-yielding bullet that redeems at par at the end of the lock-up period while entitling its owner to receive $USUAL daily token emissions during the interim—more on this later. Holders of $USD0++ can opt for waiting or for early redemption either directly with the protocol (via a floor price mechanism—more on this later) or through secondary market trading. Currently, $USD0/$USD0++ is the largest (incentivised with up to 10.5% of $USUAL token supply) pool on Curve with c. $230m, of which 93% is $USD0++, allowing swaps at c. 94c.

The particular issue of early redemption pricing has sparked significant sensitivity in recent weeks. While Usual documentation suggests in several points that $USD0++ should trade around par with $USD0 from an economic standpoint—also supported by mechanisms such as the Parity Arbitrage Right, both economic theory and observed team behaviour have indicated otherwise.

The economic theory → According to Usual’s statements related to par trading, $USD0++ yields should always at least compensate for the time value of money over the 4-year bonding period, given that the protocol’s underlying fees are tied to prevailing risk-free rates through eligible collateral. However, this claim is, at best, overly simplistic for a few reasons:

Yield leakage: there is a non-trivial loss between the discount rate and the observed asset yield due to liquidity costs and trading frictions, at c. 100-150 bps

Discount vs. hurdle rate: the present value of a crypto (or any other) investment is determined by an investor’s prevailing cost of capital rather than the risk-free discount rate, and the internal cost of capital of a crypto investor is almost certainly much (much!) higher than the risk free rate

In other words, the premise of parity secondary trading between $USD0++ and $USD0 hinges on whether the additional $USUAL yield (generated from seignorage earnings and market token multiples) can effectively bridge the gap between investors’ elevated cost of capital and the protocol’s organic asset yield. This critical relationship should form the basis of any value analysis.

The introduction of a dynamic floor in Usual’s documentation has been a late addition, as per The Block, sparking heated debate. Prior to this change (and during Usual’s pills/ points campaign) all documentation and market comms suggested the team’s commitment to supporting a parity swap. While, as discussed earlier, strict parity is impractical from an economic standpoint, secondary DEXs kept trading around par. The inclusion of a dynamic floor introduces a mechanism to provide a baseline price for $USD0++, ostensibly to reflect its time value. The initial floor, set at 87c, seems designed to align the bond’s price dynamics with those of a government ZCB, where pricing accounts for the time value of money based on a risk-free rate. However, as previously discussed, this approach holds limited relevance for $USD0++ given the higher cost of capital and unique dynamics within the crypto market, and most probably has the main intention of discouraging liquidity retrievals. Despite this theoretical alignment, the market’s reaction was brutal. The announcement triggered significant backlash on X, and widespread behind-closed-doors criticism among investors. Secondary markets quickly adjusted, trading at levels still considerably above the 87c floor but still below prior parity expectations.

Some of the problems, as many on X have pointed out, lied in misalignments and poor timing:

Inconsistent pricing at issuance: while the protocol introduced a floor price for $USD0++, it continued to allow at-par issuance, raising questions about why dynamic pricing wasn’t applied consistently to new issuances

Disparity in lending markets: $USD0++ was priced at a 1:1 ratio in some lending markets, meaning that even if considering an LTV in the market of 86% for the collateral asset (suggesting that lending curators were not crazy enough not to implement a failsafe for the repricing) a lot of leverage looping could have been executed to aggressively farm $USUAL—a leverage-loop strategy for which the pool curators are charging a nice 10% management fee

While critiques underscore concerns about transparency and coherence in the protocol’s approach to pricing, fuelling skepticism and rage, I have personally a different view, deeply rooted in pragmatism and life experience: if you are aping into a 200% returning levered strategy, you should do your homework and know the risks (and volatility) you are underwriting. I have other views on the topic, but I’ll keep them to myself. What I can say, however, is that given the irrelevance of risk-free discounting for crypto investors and the critical importance of a seamless 1:1 mint/ redemption process for staking/ unstaking for the Usual user experience, there were likely better ways to approach and execute a liquidity retention strategy. A more effective approach might have been to implement very aggressive fees in the form of $USUAL burning for unstaking or early redemption rather than relying on $USD0-based repricing. However, this is a discussion for hindsight.

While the protocol (team) retains the ability to buy back $USD0++ liabilities to support their price in the secondary market, this capacity remains closely tied to the size of the protocol’s equity, which must be robust enough to absorb shocks, and ultimately, to the price of $USUAL tokens. It is unclear whether sustaining the capital structure through gating and/ or equity ($USUAL) rather than liability ($USD0++) buybacks would be the more rational approach. Investor concerns have been raised regarding shifting strategies and vague communication about the team’s capacity to execute these measures. However, any rational investor should anticipate this behaviour, as the entire value proposition of Usual hinges on asset stickiness and capturing liability seignorage. Flexibility in approach is not just pragmatic but central to the protocol’s design.

Phase 3 & 4: Equity Emission & Emissions Retention

As noted, to compensate $USD0++ holders for the time value of their money, the protocol issues $USUAL tokens according to a monotonically decreasing asymptotic curve, incentivising early bonding. A significant portion of total emissions (45%) is allocated for these rewards. Importantly, the team (the DAO) retains discretion to adjust the allocation of emission brackets, with the exception of $USUALx and $USUAL*, which are both fixed at 10%.

According to the documentation, $USUAL tokens derive value for investors primarily from their ability to be staked as $USUALx. This staking mechanism allows holders to participate in governance (a relatively minor incentive as we know) and share in redistributions of protocol reserve revenue. Additionally, $USUALx stakers can accelerate emissions, gaining access to an extra 10% allocation bucket. Given the prevailing irrelevance of cashflow-based market rationality in tech (and especially in crypto) the primary value driver for $USUAL tokens lies simply in market pricing. Whether the pricing may reflect underlying cash flows or be driven by external metrics, such as TVL, listings on major exchanges like Binance, or overall liquidity flows, is most probably irrelevant for the holders, but something that we will nonetheless analyse later. Following its launch, the $USUAL token achieved a free-floating valuation of c. $600m, though it has since decreased to around c. $275m. The fully diluted valuation, which pessimistically assumes the market is pricing in full asymptotic emissions, currently exceed $2b, representing a TVL multiple of more than 1x even after the recent market corrections.

Phase 5: Seignorage

As with any stablecoin or abstract capital structure, the issuer’s primary ambition is to minimise liability costs by providing additional utility to liability holders—e.g. payment or settlement functionality. This principle underpins the entire concept of modern money issuance: the issuer is able to minimise the costs of its liabilities significantly below the risk free rate capturing the spread between those liabilities and the (hopefully sustainable) reserve asset yield. In banking, this spread is further amplified through implicit leverage—commonly referred to as the Common Equity Tier 1 ratio in Basel. In Usual’s case, seignorage would be achieved by expanding the volume of free-floating, non-yielding $USD0—a very difficult and laborious task which is outside of the scope of this analysis. This expansion would allow for a greater yield-per-unit to be distributed to $USUAL token holders. The critical question is how much of this expansion is implied by current market pricing and value movement—a question that forms the final piece of our value analysis.

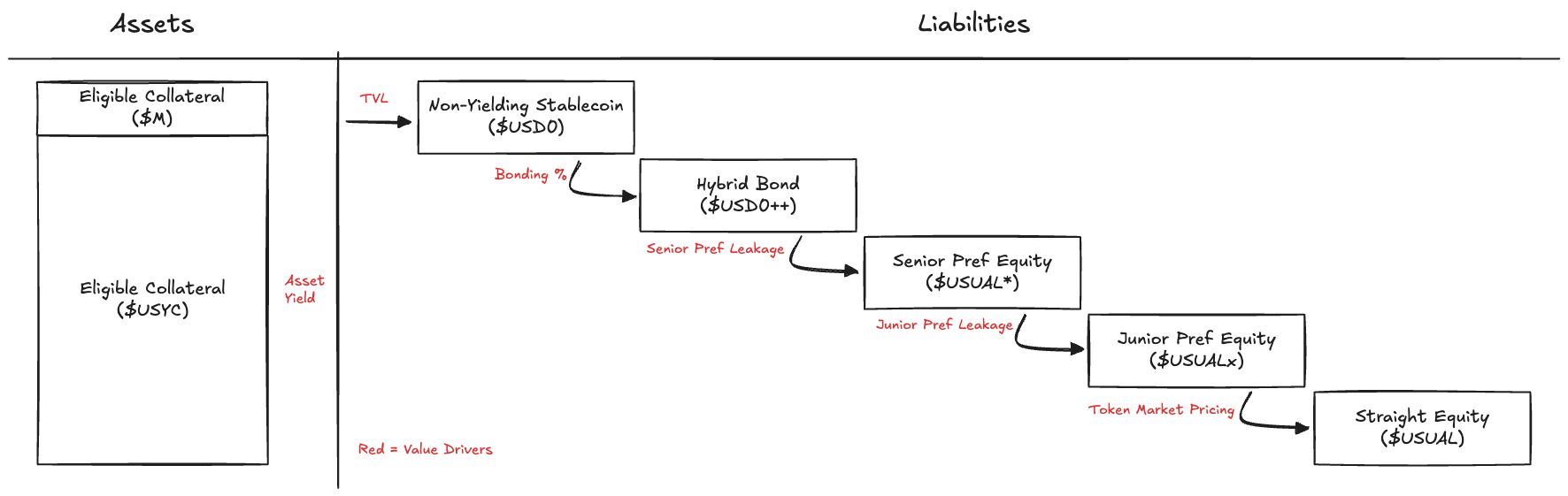

We can have some fun in depicting the complex Usual universe under a capital structure perspective.

Usual: a Value Framework

At this point, we have all the necessary elements to construct a value framework for capital deployment in the Usual protocol. Nota bene: my assumption of rationality is not naive—it serves as a useful mental model to evaluate (a) how aggressive the underlying assumptions we are underwriting truly are, and/ or (b) the extent to which we are relying on market irrationality to sustain our value thesis. This observation is not limited to Usual; it applies broadly across similar contexts and especially in crypto.

Before we proceed, a few key assumptions:

Full bonding period commitment: it is rational to assume that a capital deployer remains invested for the entire bonding period

No additional dilution: there will be no further token-dilutive incentivisation programs introduced during or after the analysis period

Constant revenue sharing: revenue sharing parameters remain unchanged throughout

Stable asset composition: asset composition, and therefore also underlying expected yields, remain consistent

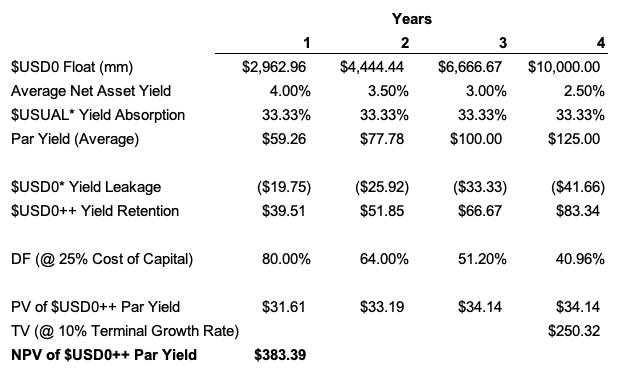

Below, I share my central value investment case, that assumes a present fair valuation for the $USUAL tokens of $383.39m, which is 27% below the current floating market cap or 5.5x less than the implied fully diluted valuation. The valuation, clearly, is based on several assumptions, but you can see how I think about it below.

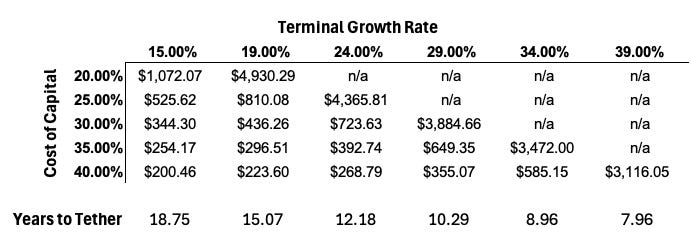

Given the heavy assumptions and the substantial dispersion of possible outcomes, a static cash-flow-based value analysis becomes largely irrelevant as a standalone tool, and it holds value only insofar as it serves as a guide to assess success. For this reason, I propose reframing the question: based on a deployer’s cost of capital, how many years should it take for Usual to reach Tether’s scale and justify its current fully diluted market valuation? This approach aligns more closely with the practicalities of long-term valuation and helps quantify the growth trajectory required for Usual to achieve market credibility relative to its main peer.

Now that we have all the elements to assess value ahead of capital deployment, it’s up to investors to decide which game they want to play. They could opt for a conservative, Graham-esque value-based approach—but then honestly why are they here?, adopt the perspective of a growth-oriented investor—assigning a specific probability to Usual’s ability to execute an aggressive vampire attack on Tether through its value distribution model, bet on insider alignment as an early contributor—through $USUAL* which we haven’t discussed here, or embrace the role of a trader navigating market sentiment.

One piece of advice, though: if you’re betting on market irrationality, don’t get surprised (or worse pissed off) when that irrationality swings back and slaps you in the face before you can get out.