# 14 | I Have Summarised the Most Recent CBDC Experiments So You Don't Have To

Wholesale, X-Currency, and Even Retail CBDCs: the BIS Is Trying to Square the Circle

This is another issue of Dirt Roads. Those are not recaps of the most recent news, nor investment advice, just deep reflections on the important stuff happening at the back end of banking. The time we are sharing through DR is precious to me, I won’t make abuse of it.

Here’s What Central Banks Have Been Doing Lately

On the 10th of September Benoît Cœuré, Head of the BIS Innovation Hub, was invited to speak at The Eurofi Financial Forum in Ljubljana. In all honesty, I used to get immensely bored during the fora I attended; I found them excessively focused on rituals and self promotion rather than substance, and I have always at least tried to remain a man of substance. Mr. Cœuré’s topic of discussion for the day, however, was one the whole political-monetary-financial-tech-crypto community had been talking about for the previous couple of years: Central Bank Digital Currency, or CBDC.

Here on Dirt Roads we have already discussed CBDCs in early July - the title of the post, The Dangerous Ambition Behind CBDCs, insinuated my concerns. We are now in the middle of September and the dust around stablecoins and crypto assets in general hasn’t in any way yet settled. Coinbase, listed on Nasdaq with a c. USD 65b market cap, even decided to go all-in against the SEC on it - you can click below.

I believe it is the right moment to write an update on what has been going on in CBDC-land. In a spree of generosity I decided to put it all together for an efficient fruition. I am sure this is good karma and that some, in the political-monetary-financial-tech-crypto community, will appreciate.

The Eurofi Financial Forum Speech

In Ljubljiana, Mr. Cœuré’s speech resembled a call to action rather than a balanced, thoughtful, analysis of the most technological developments involving money. It is probably the destiny of conservatism to go through long phases of stasis followed by short bursts of reactive energy. If Facebook of the early days adopted the move fast and break things motto, that of the BIS these days should then be storm ahead no matter what. The tone of the speech was inequivocabile. Below a few extracts - emphasis as usual is mine:

Money is at the heart of the system and it has to continue to be issued and controlled by trusted and accountable institutions which have public policy – not profit – objectives. […]

Yet the world is not returning to the old normal […] and the tech-savvy generation will soon dream about money and payments for the metaverse. […]

Why do we need to know where are we going? Because today, the financial system is shifting under our feet. […]

Banks are worried about the implications of CBDCs for customer deposits. Central banks are mindful of these concerns and are working on answers. They see banks as part of future CBDC systems. But make no mistake: global stablecoins, DeFi platforms and big tech firms will challenge banks' models regardless. […]

Will the new players complement or crowd out commercial banks? Should central banks open accounts to these new players, and under which regulatory conditions? Which kind of financial intermediation do we need to fund investment and the green transformation? How should public and private money coexist in new ecosystems – for example, should central bank money be used in DeFi rather than private stablecoins?

I could go on but you got the idea. If I had to summarise: central banks are worried about losing control of the monetary transmission mechanism and oversight of systemic financial risks, while commercial banks are afraid of not having their reason to exist as creditors and money multipliers. The BIS made it clear they are aware of those concerns, but nonetheless confirmed their intentions to move on, and fast.

Although they do not really know how to do it, they have at least identified the key characteristics CBDCs should have to be viable alternatives for the public:

Ease of use

Low cost

Convertibility

Instant settlement

Continuous availability and high degree of security

Resilience

Flexibility

Safety

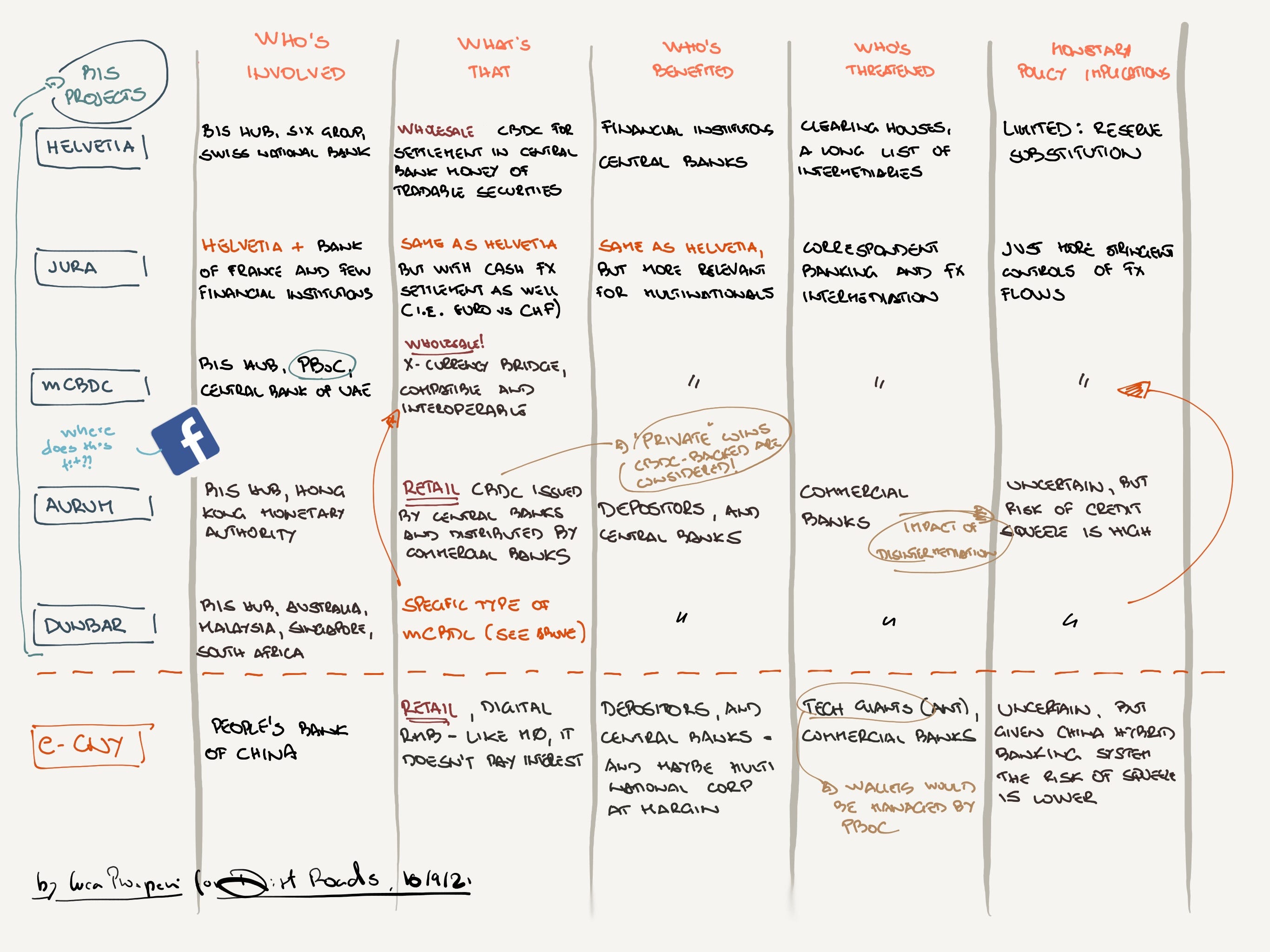

Consultations with various stakeholders have started around a few alternative projects - although I didn’t find evidence that current stablecoin issuers (Coinbase, Circle, Maker, or even Bitfinex) have been involved. The BIS cites five key CBDC projects currently in test phase, so I have summarised them on a one-pager - with a few more details to follow. They are not BIS-backed, but I added the PBoC e-CNY project and Facebook’s Diem in the mix. I have put together a cheat sheet you can print.

My Take

→ The BIS ambition seems more rhetorical than practical at this stage, with most projects not impacting the core business of today’s financial institutions - if we exclude Aurum.

→ Non-institutional use cases are almost zero - if we, again, exclude Aurum and e-CNY; it seems that the BIS wants to maintain the banks’ gatekeeper position, but I am not sure for how long this can be done - look at DeFi these days.

→ There’s an understandable aversion to develop a full-blown retail CBDC, with only two projects trying to do it - again, Aurum and e-CNY.

→ Emphasis remains on international settlements, both PvP and DvP, for cash and non-cash settlements.

→ China maintains a keen interest in at least two projects out of five, in addition to e-CNY.

→ Central banks are trying to minimise monetary policy implications, with a simple substitution of reserve balances for w-CBDC for project Helvetia, and a non-interest paying nature for retail CBDCs.

A Deeper Review of the Current CBDC Projects

For the detail oriented, I have put together a longer review of the main CBDC projects currently backed by the BIS, and linked the key online sources where to dig deeper.

(1) Project Helvetia: Settling Tokenised Assets in Central Bank Money

Who’s involved. BIS Innovation Hub Swiss Centre, SIX Group AG and the Swiss National Bank.

What’s that. Two different proofs of concepts: (i) issuing a novel wholesale CBDC (w-CBDC), and (ii) building a link between SDX (SIX digital exchange) security settlement and the existing payment ecosystem. It would provide settlement in central bank money for tradable securities, restricted to banks and financial institutions.

Who’s benefited. Financial institutions mainly, thanks to a significantly reduced counterparty risk in transactions and probably reserve requirements. The central bank as well, given much higher visibility on transactions with a positive impact on system risk.

Who’s threatened. A long list of financial services providers, clearing house, compliance and AML platforms, etc.

Monetary policy implications. Very limited, such w-CBDC wouldn’t be expansionary.

(2) Project Jura: Cross-Border Transactions

Who’s involved. BIS Innovation Hub, Swiss National Bank, Bank of France, and private sector consortium1.

What’s that. issuing two wholesale wCBDCs for cross-border settlements of cash transactions and digital financial instruments to financial institutions. Settlement will happen through Decentralised Ledger Tech (DLT) testing delivery-vs-payment of a financial instrument vs. euro wCBDC and a payment-vs-payment of Euro wCBDC vs. Swiss franc wCBDC.

Who’s benefited. Multinational corporations, financial institutions and central banks mainly.

Who’s threatened. Correspondent banking, and the FX intermediation space broadly.

Monetary policy implications. More stringent controls of international flows.

(3) Project mCBDC: Multiple X-Currency Bridge

Who’s involved. BIS Innovation Hub, People’s Bank of China, Central Bank of UAE.

What’s that. Multi-currency bridge for cross-border payments for payment-vs-payment instant wholesale transactions. Challenge is interoperability, achieved through either (i) compatible CBDCs, (ii) interlinked CBDCs, (iii) single system for CBDCs - basically a worldwide CBDC. Below I added a table on the approaches.

Who’s benefited. Multinational corporations, financial institutions and central banks mainly - not a surprise the PBoC is in the mix.

Who’s threatened. Correspondent banking, and the FX intermediation space broadly.

Monetary policy implications. More stringent controls of international flows.

(4) Project Aurum: 2-Tier Distribution of Retail CBDC

Who’s involved. BIS Innovation Hub, Honk Kong Monetary Authority.

What’s that. A retail CBDC issued by central banks and distributed through commercial banks and service providers. Two alternative approaches are investigated: (i) hybrid CBDC, and (ii) private CBDC-backed e-money.

Who’s benefited. Depositors - reduced credit risk, central banks - more control of the monetary levers, some tech provider (Facebook?).

Who’s threatened. Commercial banks - it is not great to de facto lose a big chunk of the business today and become mere payment providers. Also, not sure what will happen for P2P payments once CBDCs are distributed. This is the most aggressive form of CBDC; I have discussed this at length here.

Monetary policy implications. Uncertain. Enhanced control of the monetary multiplier, but risk of a credit squeeze due to disintermediation.

(5) Project Dunbar: International Settlements Using Multi-CBDCs

Who’s involved. BIS Innovation Hub, Reserve Bank of Australia, Bank Negara Malaysia, Monetary Authority of Singapore, South African Reserve Bank.

What’s that. A shared platform (i.e. a single CBDC ecosystem - model 3 in the table above) for cross-border transactions using multiple CBDCs for financial institutions.

Who’s benefited. Multinational corporations, financial institutions and central banks mainly.

Who’s threatened. Correspondent banking, and the FX intermediation space broadly.

Monetary policy implications. More stringent controls of international flows.

(6) Project e-CNY: Digital M0 For Retail Distribution

Who’s involved. The People’s Bank of China and authorised credit institutions.

What’s that. Digital version of fiat currency, issued to retail users through a 2-tier system that includes PBoC and authorised credit institutions. It will exist alongside physical RMB, with the ambition to progressively substitute it. e-CNY would be interoperable, domestically and internationally, and leverage DLT. In the current framework e-CNY acts as a substitute of M0, and pays no interest to holders - with the intention of reducing competition with bank deposits.

Who’s benefited. Depositors - reduced credit risk, central banks - more control of the monetary levers, multinational corporations - thanks to enhanced interoperability.

Who’s threatened. Tech giants such as Ant, that risk disintermediation of their electronic wallets. Commercial banks - even if the Chinese hybrid private-public banking model makes this no new news.

Monetary policy implications. Uncertain. Lower risk of a credit squeeze given the hybrid private-public banking model.

Special Mention: Diem

Although the Diem project is sponsored by Facebook and not by a central bank, an update post on CBDCs couldn't be complete without a special mention of where Libra, sorry Diem, stands. It seems that Facebook pivoted quite radically from their original idea, making the vision behind their stablecoin more palatable to regulators, up to the point that Christian Catalini, Diem’s top economist and old university buddy of mine, has stated that Diem is intended to be a stand-in for CBDCs to be monetised as a payment infrastructure. Four key changes have been made to the original Libra project:

Single-currency stablecoins are offered beside the original multi-currency alternative, to avoid interfering with sovereign monetary policies

Introduction of an official compliance framework for CFT, AML, and financial intelligence purposes

Abandoning Libra’s original permissionless nature

Building strong guidelines governing the reserve assets that back Diem

Facebook’s hope, as stated in their whitepaper, is that CBDCs could be directly integrated with the Libra network, removing the need for Libra Networks to manage the associated Reserves, thus reducing credit and custody risk. They want, in other words, to partner with governments and central banks in order to provide effective international payment rails where transactions would be executed. I believe this move to be relevant, and connected to the explosion of the interest around Buy Now Pay Later (BNPL) companies recently - e.g. Klarna, Afterpay, Affirm, GreenSky. Alex Rampell, from VC giant a16z, summarised this wonderfully in a twitter thread (below).

Why are BNPL providers valued so highly? Hint: it is not for the credit spread. BNPL companies are building alternative payment rails that can connect the manufacturer to the merchant and ultimately the consumer. This is relevant in both directions. First of all, BNPL new rails are able not only to provide simplistic visibility of the money transfers but also data about customer behaviour, similarly to what happens for clicks - and a purchase is much more informative than a click. Secondly, and this is even more relevant, those new rails would allow manufacturers to act directly on pricing or payment plans to market their products, with full control and visibility. This makes purchases fully observable, influenceable, and programmable.

It is not only about payments, it is about observing and manipulating value. While traditional BNPL players are aiming at building those networks by signing up consumers and merchants at an accelerating rate, Facebook is instead trying to do so by partnering directly with the money production factories.

Innovating is a communal effort. If you have great ideas you want to explore together, great companies that should be on Dirt Roads radar, or topics you would like to co-author on DR, please feel free to reply to this email or contact me on Twitter.

The private sector consortium includes Credit Suisse, Natixis, R3, SIX Digital Exchange and UBS.