# 22 | I'll Be Your Mirror, Reflect What You Are

From the Earth to the Moon (III)

This is another issue of Dirt Roads. Those are not recaps of the most recent news, nor investment advice, just deep reflections on the important stuff happening at the back end of banking. The time we are sharing through DR is precious to me, I won’t make abuse of it.

The Terra Money Tetralogy:

Episode I: Terra Money: a Primer

Episode II: Demystifying Anchor, Terra Money-Spinner

Episode III: I'll Be Your Mirror, Reflect What You Are - this post

Episode IV: ?

Terra is a sovereign economic system aimed at issuing, managing, and manipulating financial value. Terra is also an observable pegged monetary system where the volatility within its currency $UST (vs. the pegged sibling, the dollar) is transferred from currency holders to the system’s equity holders: treasury, domestic companies, $LUNA token holders in general. The Anchor money-market protocol acts as the entry gates for anybody aiming at interacting with the Terra sovereign financial hub. Anchor’s force of attraction towards Terra is strong, but like a dying star Anchor is consuming itself and one day its cosmic fuel might finish unless huge value will start being generated within the Terra ecosystem.

The fact that one thing doesn’t make sense comes often with a visual feeling, a taste of something missing. The problem is that, most of the times, a general analysis of what makes sense might disagree with what a local one would conclude. The mental structure is the same, and what differs is the assumptions. Even the consistency of our entire mathematical system is based on a set of unprovable assumptions called axioms - ed. the ZFC. If you tried to go one step back and literally prove one of those axioms, than you might need another set of axioms, or maybe entirely another system, to make it work. It is the incommensurability of such research for a provable truth that has been so well described by Gödel, Khun, and Becker. For a salmon swimming upstream during a few days, that river might well be flowing in eternity. For a mountain, it is different. We humans get continuously stuck in this inconsistency. We can think symbolically but must live locally, and although we try to forget it when we illude ourselves of an eternal life, sometimes reality catches up. If we would expand our perspective enough, we could logically state that pretty much everything we observe or do doesn’t make any sense at all.

If I had enough self-confidence this would be the argument I’d use with anybody calling the DeFi revolution, as a whole or in its sub-components, a Ponzi scheme. What isn’t? Isn’t your life a Ponzi scheme? Won’t you have to give back to the universe what you have been acumulating in a way or another? But I don’t have that kind of self-confidence, or wisdom. In the long run, as Keynes said, we are all dead. As investors, or even mathematicians, we should focus on the local rather than the universal. Things don’t need to keep making sense for ever to succeed, they need to keep convincing people they do for long enough to make investment sense. We should all take ourselves less seriously if we want to make some money.

Is Terra a Ponzi then? Does it make sense? Short answer is: it might. And it might because of a rough gem that has been nursed at the centre of the ecosystem, protected against external attacks. That gem is called Mirror, Terra’s TradFi greed magnet. If Mirror won’t be successful, we might revisit our conclusions on whether the whole castle will stick around for long enough to make us all rich.

Mirror: Tesla’s Hedonist Dream Incarnated

“I weep for Mirror (ed.), but I never noticed that Mirror was beautiful. I weep because, each time he knelt beside my banks, I could see, in the depths of his eyes, my own beauty reflected” - Tesla stock, Nasdaq Stock Market, New York City, Real World.

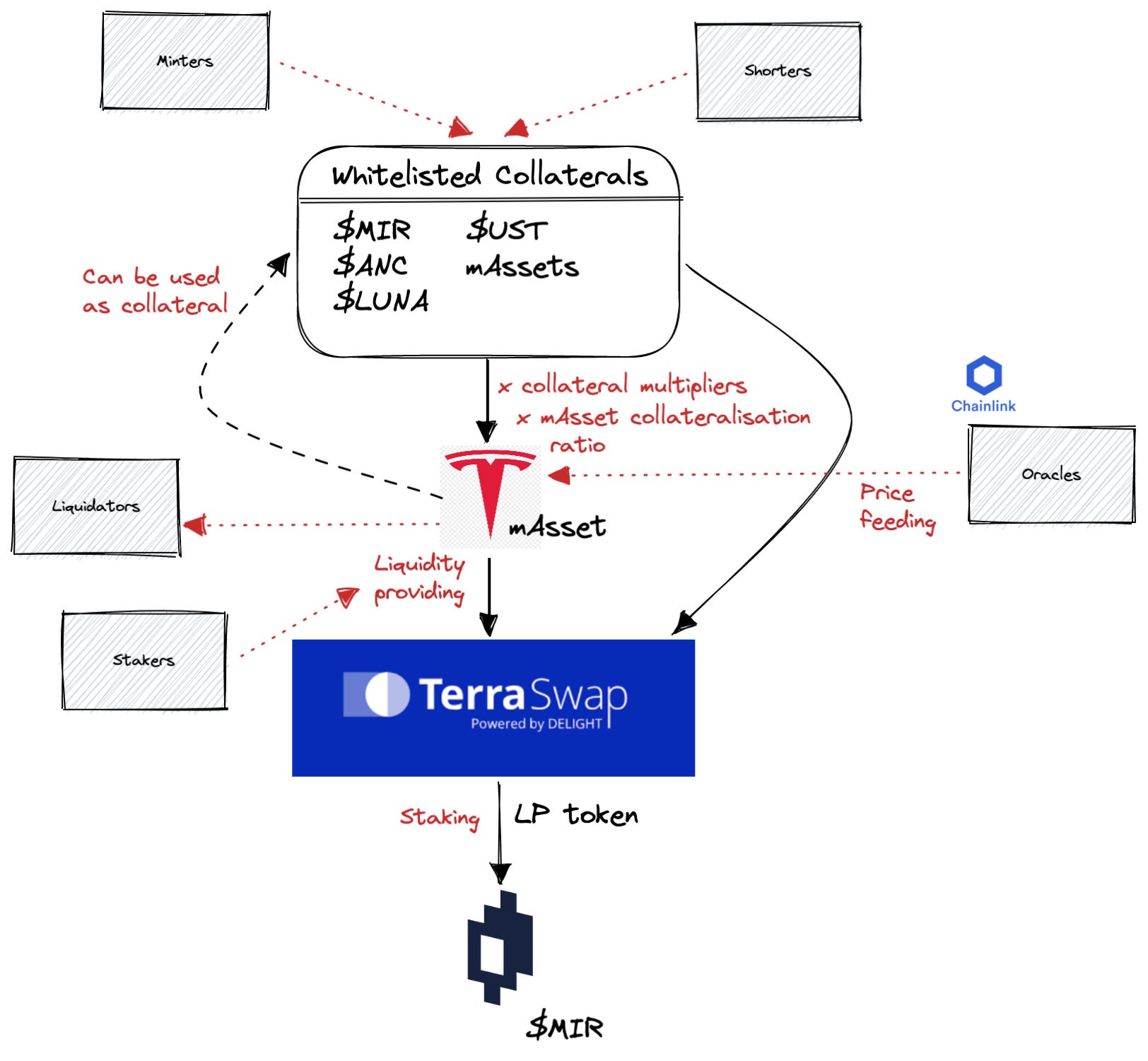

What is Mirror? Mirror is a sovereign, decentralised, internally regulated, unbounded, agnostic, value exchange protocol. Every action, and actor, within Mirror embeds all those aspects, and all those aspects are enforced by governance through voting in the usual one-token-one-vote system. There are a few primitive actions we should get acquainted with before anything else.

Minting → An actor enters into a Collateralised Debt Position (CDP) where mirrored assets - mAssets, i.e. synthetic copies of a set of whitelisted securities traded somewhere else, get minted in exchange for a parametric amount of collateral that must be held within certain thresholds. The required collateral amount is determined by multiplying a collateralisation ratio (specific of the mAsset) and a multiplier - specific of the collateral used. Punishment is liquidation through a discount auction. Mirror gets a 1.5% fee every time a CDP is withdrawn, and such fee is sent to the staking pool.

Liquidity providing → In proper AMM-DEX style, those mAssets can be placed, together with another Terra asset, in a Terraswap liquidity pool in exchange for a fee share, and for some old school farming yield. LPs get traditional LP tokens representing their portion of the pool. Price discovery, for what pertains Mirror, happens within those pools.

Price feeding → Although internal price discovery happens within the liquidity pool, those synthetic assets have an external (centrally regulated) exchange venue. Whitelisted oracles provide periodic (non real-time) updates on prices. The availability of those prices is necessary for new open market operations like minting, shorting, or liquidating.

Shorting → An approach similar, but inverse, to minting can be used for shorting. An actor enters a CDP position, mints an mAsset, and sells it immediately to get a sLP token - nomenclature is awful I know. When the oracle price is lower than the Terraswap equilibrium price, those sLP can be staked for a reward - below. De facto, shorters get temporarily remunerated every time the price moves south. The experience, however, is cumbersome.

Staking → Tokens provided to users (LP - liquidity, sLP - shorting, $MIR - Mirror’s customary governance token) can be staked to earn further $MIR. The $MIR tokens provided in exchange for staking LP and sLP inflate the $MIR pool, whereas the rewards for staking $MIR derive directly from accrued protocol fees - and are therefore non-dilutive. As usual, staking represents an extra incentive for users to get involved, although such incentive doesn’t come for free but in the form of value dilution for $MIR holders. The protocol’s ambition, like in many other cases, should be of progressively converting through policy changes dilutive staking into non-dilutive $MIR bonding. As we all know well however, yield farming is addictive and microdosing it is difficult.

But What Exactly Are mAssets?

A few months ago here on Dirt Roads I indulged into a convoluted philosophical description of money - here. One I still firmly believe in. Money is a measurable transposition of systemic uncertainty, and the monetary base within a system, I argued, could be grown sustainably only vs. a growing and not-too-correlated set of uncertainty sources. A lack of uncorrelated sources of uncertainty, or entropy, is DeFi’s cardinal sin: with trading, or actually trading on the margin, being the main use case within DeFi nowadays, there are incredibly high correlation levels across most crypto-assets. Growing the footprint of a system in such shape would be like building on sand: it wouldn’t take much to bring the castle down. I firmly believe this to be a temporary phenomenon: there is no infrastructure out there that is better-suited to trade an incredibly vast pool of uncertainty sources than DeFi. Real-world assets financing, prediction markets, smart insurance products, those are just timid examples of what can be onboarded. Soon we will be able to tokenise and exchange many more sources of uncertainty - and value.

In the meanwhile, there is money to be made, and Terra decided to bootstrap growth by accessing the biggest, readily available, uncertainty market there is: the stock market. The various components of the Terra ecosystem available today - its bridges, money markets, crypto-banks, payment systems, are all functional but not fundamental to Terra’s vision. Through Mirror, Terra is instead trying to import the most powerful and abundand raw material existent to turbocharge its growth, and wants to do it without asking permission to anyone. Unsurprisingly, hijacking a regulated market without pissing off the regulator wasn’t going to happen.

In June, Mirror launched its v2 with some powerful updates. Governance changes were implemented to incentivise a more active participation, new collaterals were included in the whitelist, and some assets not yet IPOed could now be minted and traded. As usual, in the spirit of total modularity, other protocols started building on Mirror’s platform.

But Terra is not only trying to funnel blocks of uncertainty away from the Nasdaq; they are trying to do the same to DeFi’s main liquidity pool, Ethereum. A bridge called Shuttle facilitates transfers of assets between Terra and other blockchains. $MIR tokens and mAssets, after being minted in Mirror through the mechanism described above, can be placed in Ethereum liquidity pools on Uniswap or KuCoin.

Providing liquidity for Twitter mirrored-shares on Uniswap yields a 64.88% APR at time of writing, in exchange for some of the TWTR upside - read impermanent loss. Twitter mirrored-shares could be minted on the margin in exchange for Terra-native collateral, such assets can be placed in Terraswap liquidity pools in exchange for Terraswap LP tokens, those LP tokens can be staked within Mirror for $MIR rewards, and $MIR placed into both Terraswap or Uniswap liquidity pools for some extra APY. There is a lot of risk amplification going on, and it’s no surprise that the SEC doesn’t like it when such activity is a) open to every possible type of investor out there, b) is tied to prices of regulated securities, and c) has no central party you can switch off if you need. Also, things get very complicated very fast. Mirror is Robinhood on steroids galopping in the dark planes of the blockchain.

Boyhood

The other, although today less pressing, question that the SEC should ask itself - related to both the Mirrors and the Robinhoods of this world, is whether those trading venues have any use for the primary issuers, i.e. for the corporations that use trading venues to raise funds to be put at use. Do they add value Or better, do they make sense? If you strip out all the bells, Mirror and others are collateralised betting machines, although the discussion for a protocol such as Mirror at the core of a sovereign monetary system is a different one. But, again, there might be several development phases ahead.

Phase 1: Terra is Macau. Mirror is just a well-functioning collateralised betting machine, it attracts several ancillary services but ultimately doesn’t add much value beyond fun, wealth redistribution, and maybe tax evasion - usually at the expense of the weak. Regulators don’t like it because they should want to protect the weak.

Phase 2: Terra is Bermuda. Mirror’s well functioning, coordinated governance mechanism, is incentivising liquidity to leave traditional markets in bulk. The movement starts making a dent in domestic liquidity pools. Regulators don’t like it because there is often tax avoidance involved, and because a reduction of liquidity in traditional trading venues weakens price discovery and market efficiency.

Phase 3: Terra is Singapore. The amount of liquidity available within Mirror actually incentivises Terra-native businesses to seek liquidity by directly listing on the marketplace, in a permissionless way. The whitelisted collateral pool expands and those businesses can use tokenised assets as pledge, although naked uncollateralised listings might go online as well. Regulators don’t like it because they are losing further control of the financial intermediation industry, with effects on jobs.

Phase 4: Terra is New York City. Not only Terra-native, or even crypto-native, businesses use Mirror to mint risk capital, but also so-called real-world ones. Mirror becomes one of, if not the, most relevant capital raising platforms within DeFi. Terra’s accomodating and transparent monetary policy, coherent direction of travel, and technological transparency boost growth further for the benefit of all. Regulators hate it.

In answering the SEC, Terra founder Do Kwon stated clearly that Terraform Labs couldn’t switch off Mirror even if they wanted. And they don’t. The SEC wasn’t too sympatetic with his views, and warned users that they should start questioning how truly decentralised decentralised protocols are. This is a common semantic problem behind the rethorics of the decentralised economy. Looking at the final $MIR token distribution (below) doesn’t help because, as usual, many actors do many things - they are governance token holders, market makers, protocol users. It is early days for a deep analysis of the governance dynamics of a DAO.

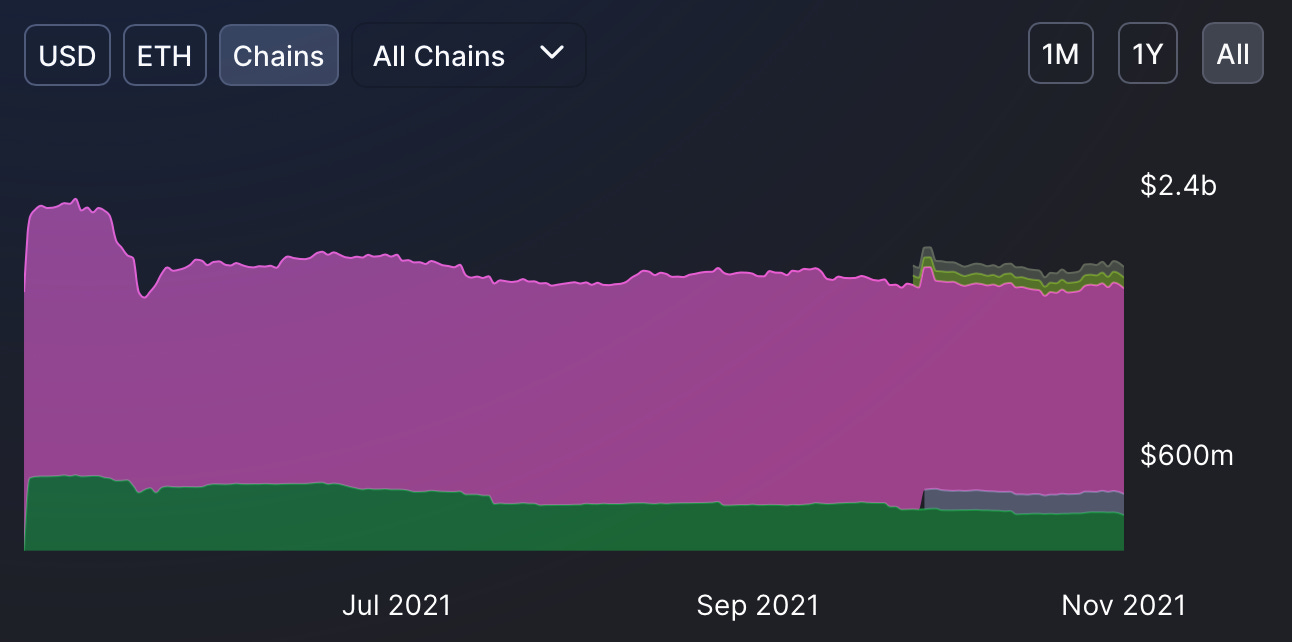

Mirror’s success has been huge in absolute terms, but mixed when adjusted for DeFi typical growth rates. The protocol’s total value locked has been stable beteeen $1.5-2.0b over the last months. There might be multiple reasons: regulatory pushback, clear competition from TradFi / tech-friendly trading platforms, high slippage and other inefficiencies, or simply the fact that there was no need to acces other sources of uncertainty to trade and speculate during the last months in DeFi. The next crypto-winter might change things.

Last Words

The ambition, again and again, is composability. Terraform is seeking partnerships with front-end user interfaces - read WSB, and more sophisticated use cases can be build on top of the mAsset primitives. We talk basketing, indexing, leveraging through collateralisation, product structuring, all this in a permissionless, transferable, composable way. It might work but at the bottom of everything, let’s not forget, the reflection won’t be more attractive than the subject staring in the mirror.