# 9 | Flatland: Minting Money Out Of Radical Uncertainty

MakerDAO's Real World Hunt For New Sources of Entropy Is Only the Beginning

This is another issue of Dirt Roads. Those are not recaps of the most recent news, nor investment advice, just deep reflections on the important stuff happening at the back end of banking. Because banking is nothing but a pragmatic translation of our ability to imagine what hasn’t yet happened, but could. The time you dedicate to read, think, and share, is precious to me, I won’t make abuse of it.

“You Ever Heard Something Called M-Brane Theory Detectives?”

Money is time, they say, but you haven’t heard it from me. They say money is the accumulation of past efforts, or the representation of future endeavours projected into the future and discounted back to today. I don’t like this definition.

Time and space are closely related, merging into Einstein’s special and general relativity. Different from the space dimension, however, time seems to have a direction of travel: the past lies behind, immutable, and the future remains ahead, uncertain. But this, too, is disputed, as it might depend on the system being analysed, and narrated. Entropy, as a measure of disorder, might well increase with time flowing in either direction. In other words, the more you distance an observer from a specific point in spacetime, the more entropy increases. Information theorists see it (entropy) as a measure of random loss of information.

I like to think of money as a measure of entropy. This updated definition is not merely academic, it is functional. We can increase the system’s monetary base by trading money for larger and larger amounts of entropy or uncertainty - we will use the two terms interchangeably, coming from more and more sources. Distance in time is only one of those sources.

It is not difficult to make, I prefer to say to mint, money. Keeping it instead, without letting the system go bust, is a different story: it is a fine exercise of balancing those same sources of uncertainty so that, instead of getting amplified, they partially cancel each other out at an observer’s arbitrary location on the spacetime hyperplane.

Diversification and Universal Love

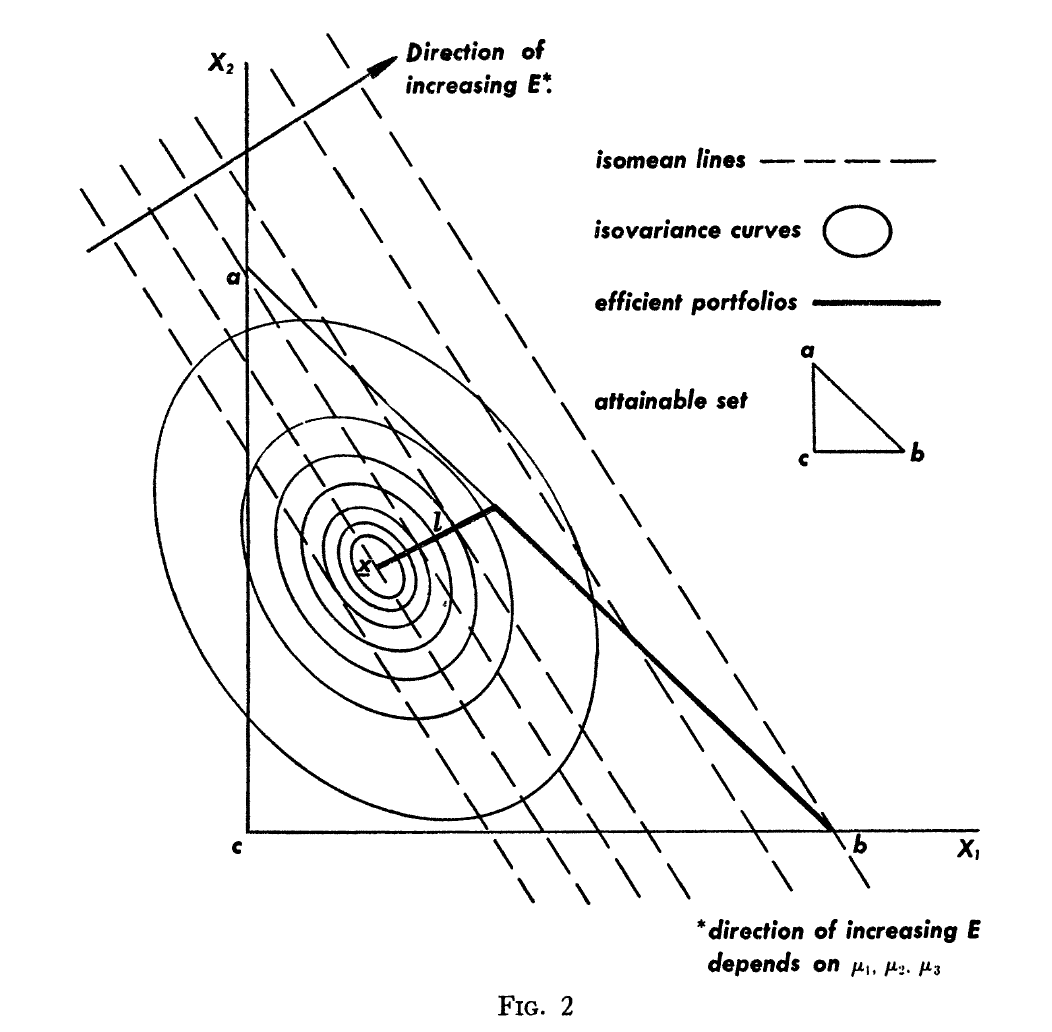

We seem to have subconsciously known this for ever. It was the commonly adopted and observable practice of diversification to inspire Markowitz’s 1952 seminal paper on portfolio selection:

The hypothesis (or maxim) that the investor does (or should) maximize discounted return must be rejected. If we ignore market imperfections the foregoing rule never implies that there is a diversified portfolio which is preferable to all non-diversified portfolios. Diversification is both observed and sensible; a rule of behavior which does not imply the superiority of diversification must be rejected both as a hypothesis and as a maxim.

[…]

The portfolio with maximum expected return is not necessarily the one with minimum variance. There is a rate at which the investor can gain expected return by taking on variance, or reduce variance by giving up expected return.

Do not ask me why investors still use DCF methodologies (with static discount factors even) to value assets, because I do not have a good answer for it, beyond guessing that it takes quite a long time to absorb what we have learned on paper into our pragmatic ways of navigating the world.

Reformulating Markowitz, humans have had an innate dislike for entropy, a desire to protect their selves in all possible alternative futures - or multiverses if you move from relativity to quantum mechanics - but please ignore this last comment.

The Birth and Near-Death of Modern Financial Services

The explosive emergence of the modern financial sector is linked to the manipulation of additional sources of uncertainty people were ready to trade. Medieval bankers started the game by trading on space distances, providing merchants with facilities to deposit and withdraw value around the world avoiding the burden of carrying any form of storage. They then progressed to trading on time distances, financing future crops and investments to gather resources or improve productivity. Then, during the 17th century the Lloyd’s Coffee House moved to underwrite a more general form of uncertainty in the form of risk-sharing contracts, or insurance.

In the second part of the 20th century, innovation in financing (and to a lesser extent insurance) allowed institutions to increment the sources of uncertainty they could mint money against, thus expanding the monetary base. At the same time, the innovation in derivative instruments helped the same agents have a better, i.e. more diversified, portfolio approach of those same sources, supporting the growth in size of those institutions.

At the beginning of the 21st, it was the under-appreciation of how those sources of uncertainty might have actually been slightly different representations of the same phenomena (i.e. of their covariance) that almost killed the same financial sector.

Today, at least in the TradFi space, there are professionals making a (very good) living by promising to expand those sources of uncertainty via strategies that do not have much in common with the large part of institutional portfolios. They call their own crowd absolute return. The mere observation that they dine in the same restaurants, date the same people, and come from the same schools, might be a good hint they are overselling the lack of correlation with the system and among themselves.

The Huge Correlation Issue of the Cryptocurrency Space

If there is one problem affecting the cryptocurrency space today, is exactly correlation.

Although use cases are expanding, for the sake of investors most crypto tokens are the representation of the same thing: the market’s appetite for the crypto space in general. Understanding the macro or technical drivers behind this appetite is the realm of the punditry, not mine.

Vincenzo Candila wrote a great paper for those who want to dig deeper in the econometrics of price behaviours of cryptocurrencies (please form an orderly queue).

The high correlation among available assets has the huge impact of inhibiting the ability to diversify among sources of uncertainty, limiting the capacity of the system to mint money. When it comes to DeFi, we are still deep in medieval times.

At worst, high correlation is not only limiting but potentially destructive for DeFi. Banks and insurance companies are not profit optimisers, as they are more worried about protecting themselves (and their capital) from the worst case scenarios. But worst case scenarios are sudden in nature, and offer little anticipation to educate decision makers in taking appropriate protective measures. Given the limited history of the crypto economy, governance tokens holders might be tempted to underestimate the uncertainty they are underwriting. MakerDAO lost money in liquidations only during a month since inception, and that also was due to an endogenous (protocol failure) rather than exogenous factor, why should correlation be considered a real threat?

MakerDAO Craves (Uncorrelated) Uncertainty

Readers of Dirt Roads know that we often refer to MakerDAO as the most important project in the crypto space when it comes to the ambition of creating proper on-chain banking (# 1 | Decentralised Banking). However, being a sound bank and minting significant amounts of money requires a well diversified portfolio of sources of entropy. Maker’s portfolio diversification is far from great.

As you can see from the chart above, ETH represents the quasi totality of token exposure ex. stablecoin. Even if we ignore the correlation of ETH vs. other tokens, Maker’s portfolio is almost entirely dedicated to lever ETH ownership. The problem has been exacerbated in the current phase of the investment cycle, pushing the protocol to purchase huge amounts of USDC to provide support to the DAI peg and with the additional effect of de-levering the balance sheet and drastically reducing revenues and profits.

Based on the current situation, the DAO doesn’t expect Maker to turn profitable in the foreseeable future. It won’t unless there is a sustained increase in collateral posting / DAI minting, and that increase won’t improve Maker’s solvency unless additional, uncorrelated, sources of entropy are found.

The DAO has gone on a hunt for those sources.

Centrifuge: Bridging Universe and Metaverse1

So Maker turned to the real world. After all, most sources of uncertainty get still financed by traditional institutions and traditional capital markets. By constructing a bridge between DeFi and real businesses both sides could benefit. On the one hand, real businesses might see increased competition among product providers and consequently better terms, and on the other crypto banks (and insurers - if we keep using ancient terms) would expand the sources of uncertainty they can mint money against while reducing their own portfolio correlation.

Centrifuge responded. The company had been trying to connect the two sides by developing the required infrastructure for so-called on-chain securitisation. The story of Centrifuge, however, has been testament of how ideas that seem obvious at the start struggle in finding traction in practice. After years of hard work, the Total Value Locked in Centrifuge’s Tinlake protocol is a mere USD 28m. Not enough to cover MakerDAO’s stated ambition of onboarding USD 300m of Real World Assets (RWAs) as on-chain collateral by the end of 2021. Nonetheless, the two have decided to partner.

New Silver was the first real world issuer to be used in Maker’s collateral vaults. The company is a tech-friendly real estate bridging financier for the US fix & flip market, with maturities ranging in 12-24 months and interest rates in the 10-13% range - not exactly the perfect candidate for a low-risk, liquid, over-collateralised protocol such as Maker. The loans, originated by New Silver, are tokenised by Centrifuge in NFT form and then securitised by Tinlake against interest bearing tokens of different seniority, NS-TIN (20% first-loss tranche) and NS-DROP (senior tranche). The senior tranche can ultimately be used as collateral to mint DAI at 6% (now 3.5%) stability fee. There are currently c. DAI 6.3m minted against NS-DROP.

Since then additional RWAs have been included as eligible collateral, for a total debt ceiling of DAI 44m. Only 14% has been used, with TVL of USD 22.5 (due to customary over-collateralisation). We are far away from the FY2021 ambition of DAI 300m, or from any relevant number for Maker. As a reminder, the amount of total DAI outstanding is currently 5.6b (if we include USDC, and 2.4b if we exclude it).

RWA Supply Shortage and the Future of DeFi

I had the pleasure of having a chat with Sébastien Derivaux, who leads the RWA effort for MakerDAO and helped me navigating the topics described above. Maker’s ultimate ambition is that of expanding the sourcing of collateral assets as well as the ways to put its balance sheet at work effectively and this, in the self contained crypto economy of our days, requires building a bridge between DeFi and TradFi. But building that bridge is proving to be expensive, and is attracting limited interest. The reasons behind this shortage of real world assets might be numerous (below, my view).

Operational complexity. On-chain securitisation is a new area and pioneers like Centrifuge have to sustain all the required exploration, education, and marketing costs.

Relative low incentives for developers and investors. Even after the end of the 2020/21 crypto summer, the time and effort of blockchain developers and investors could be highly remunerated by operating within the crypto sector without the need to migrate real world use cases on-chain - Sushiswap launched on August 28th 2020 and hit USD 150m of TVL in less than a day, and in 2021 Axie Infinity achieve north of USD 200m monthly revenues within less than six months of effective life.

Cultural gap. The languages spoken by credit originators, securitisation sponsors, and DeFi developers are radically different. The issue exists on both directions: it is difficult to educate old school practitioners on the mechanics of DeFi, and we are unsure that those mechanics (both technologically and governance-wise) will work effectively to assess risk in ultra-specialised spaces like structured credit.

But do we need real world assets to expand the sources of uncertainty against which DeFi mints money? Or are we limiting ourselves to the old tools? Entropy is agnostic, and is everywhere around us. Prediction markets such as Omen or Augur, or smart insurance projects, have been initial tentatives in this direction. The future might see a growing number of use cases natively emerging on-chain and looking for financing; today we are not in a position to predict what those use cases will be without falling into the framing trap - i.e. proposing the old as the new. There will surely be more entropy to squeeze from spacetime as long as there are agents ready to pay value to reduce those sources of uncertainty.

We can be more ambitious I believe, and bring also algorithmic, non-human, agents in the picture. Randomness is built at the roots of cryptographic technology, and if we look around there are an infinite amount of uses that would benefit from a reduction of randomness, and ready to pay money to obtain it. It remains to us to capture entropy and represent it as something tangible, marketable, and leverageable, as the Medici did in the 15th century.

Innovating is a process. It starts with sourcing ideas, and proceeds with disseminating those ideas for testing, funding and high-quality execution. For this reason, it is collegial in nature. If you have great ideas you want to explore together, great companies that should be on Dirt Roads radar, or topics you would like to co-author on DR, please feel free to reply to this email or contact me on Twitter.

From Wiki. The Metaverse is a collective virtual shared space[1] including the sum of all virtual worlds and the Internet. It may contain derivatives or copies of the real world, but it is distinct from augmented reality.

By integrating with RWAs - aren't you moving from being correlated to crypto to being correlated with tradfi instruments?

Doesn't crypto stop being a hedge against fiat?

I suspect the lacklustre demand so far for on-chain RWA securitisation is in part due to the extremely low cost of capital in the RW. Why bother with DeFi if there’s plenty TradFi sources of capital available willing to price generously? Right now Centrifuge et al. are competing with a wall of money from non-bank lenders that have stepped into the space. And mixing the two in your capital stack is hard (don’t know of anyone who’s done it).

But tbf it’s still early days. Over time I think originators will just add DeFi as another source of capital to their pool of options. Tokenising via Centrifuge is not particularly hard, and of course there’s intermediaries emerging (e.g. Fortunafi) to help with that. The cultural barrier you highlight is real, but the fintech boom in TradFi means incumbents are being quickly replaced by more tech savvy — shall I say crypto native — competitors.