# 5 | It Is Time to Redefine Risk

The Concepts of Capital, Exposure, and Leverage, Require a New Definition in DeFi

This is another issue of Dirt Roads. No financial reports analysis, no marketing material dress downs, no investment advice, just deep reflections on the important stuff happening at the back end of banking. Because banking is nothing but a pragmatic translation of our ability to imagine what hasn’t yet happened, but could. The time you dedicate to read, think, and share, is precious to me, I won’t make abuse of it.

Conversation Club: Innovating Credit Risk

Posts look good when they are final. When they start with clearly defined premises, proceed with ordered and detailed arguments and counterarguments, and reach actionable conclusions. It can’t always be so easy. Especially when you realise that something as big as the very definition of risk needs updating.

Banks create purchasing power for individuals and corporates alike. Some are good borrowers, others are not. If a bank does its job appropriately, the compensation received under various forms is enough to more than compensate the losses incurred for selecting the wrong projects to back. That’s it. A traditional bank, a pseudo-bank, a crypto-bank, a commercial lender, are all engaging in doing the same job.

Over the years, regulators and the very banks have developed a set of metrics to monitor balance sheet soundness and credit quality, and to communicate those to external stakeholders. But balance sheets have become heterogeneous and not too transparent, and those metrics have been multiplying up to the point that reading a Pillar 3 report is like interpreting a holy scripture. With the surge of DeFi banks, in an effort to “think like a bank” teams have been forcing the traditional risk monitoring framework to entities (or better protocols) that don’t have much in common with brick-and-mortar institutions.

There is a lot of merit in doing so, but the rise in relevance of DeFi banks (and many other financial intermediaries like CrossLend) demands for the development of a new, endogenous, risk management framework. Given the pro-cyclicality of some of the most robust crypto-banking protocols like MakerDAO - it should be clear by now that I am a great estimator of Maker, it might be prudent to develop such a framework before the next bull market.

This post is not a manual, but rather a call to action to start doing so.

Understanding Banks’ Raw Material: Capital

Bank’s capital is the institutional cushion able to absorb unexpected losses arising from running the business. It is traditionally sliced in tiers, from best quality capital like Common Equity Tier 1, down to Tier 2 capital. Quality is linked to its capacity to absorb losses: CET1 is considered of the highest quality since it is not redeemable by its holders, it has permanent duration, and doesn’t necessarily need to be compensated in the form of dividends (which are not mandatory). The value that bank shares have in the secondary market (its market capitalisation) is not considered capital: it has the potential of becoming it, but in order to benefit from this potential a bank should issue new shares.

This has the perverse effect of putting high-growth/ high-margin banks in a position of disadvantage vs. low-growth/ low-margin peers. Institutions with debatable balance sheet quality and low profitability, that trade at a price below their book value, don’t have to account for the market discount in the capital calculation and therefore have their regulatory solvency position overrepresented. On the other hand, high quality institutions with great growth and high profitability, trading above book value, will need to wait for those profits to materialise in order to include the market premium in their capital position unless, as said before, they decide to benefit from market hype by issuing new shares. But locking money in the bank’s coffers has opportunity costs for new investors and means that existing shareholders are giving up future value for a raw material they might never need if all things go as market expects. This is not optimal.

The enforceability of smart contracts allows DeFi banks to do better. DeFi banks too embed some form of surplus that is retained in order to absorb first losses, but differently from traditional banks this surplus is extremely thin (DAI 50m vs. 5.3b of assets in the case of Maker), making their balance sheet much more efficient. This is doable because in a smart contract construct if Maker will need to replenish its reserves MKR token holders can rest assured they will be diluted via newly minted tokens that facilitators will be incentivised to buy. There won’t be discussions with investment banks, no roadshows, no calls, no book-building. It will just happen.

DeFi banks are, in other words, structured to continuously recur to a reliable bail out mechanism where token holders step in to ensure the stability of the liability structure. There is therefore a clear case in favour of considering the token market capitalisation as part of the capital base of a DeFi bank, differently from what happens for traditional institutions. Token holders know they will be lenders of last resort for the bank, and get compensated by a forward-looking earning yield that is significantly higher than that of traditional banks. This promise, as many others, is embedded in the code of the token they have purchased.

Calculating Collateral Exposure

We have talked about capital, i.e. the numerator of the leverage ratio, so next should come the denominator: exposures. Banks underwrite promises of future (re)payments (assets), and at the same time offer similar promises to others (liabilities). Those promises are in turn backed by collateral guarantees of any kind. Quantifying the value of those collateral guarantees is the first step towards understanding a bank’s leverage and resilience. It is not an easy step. Nobody has an exact view of what is hidden on both sides of a bank’s balance sheet. Most underlying collaterals are contractual, do not have external executable valuations, and are often complexly structured.

DeFi banks do not have those issues. On the one hand, crypto-banks tend to be single-liability (the promise issued by MakerDAO is only one: a 1-for-1 soft-pegged DAI). On the other, with data available on-chain it is fairly easy to assess the availability and value of collaterals for risk mitigation purposes. Nevertheless, we should remind ourselves that we are at the infancy of lending protocols, with collateral pools limited in number and type. Things will change - Maker is already onboarding real world assets, and credit analysts will need to get comfortable in auditing code and not only interpreting lending agreements.

Another Impact on Credit Valuation: Merton Applicability

There is another interesting consequence for credit risk of the surge of DeFi - this one for the geeks. With on-chain transparency and immediate tradability of (almost) all underlying exposures, DeFi banks have finally made the Merton model relevant to value a bank’s underlying credit risk.

Under Merton’s credit risk model, the value of equity is represented as a call option on the enterprise value of the company, with a strike price equal to the value of its liabilities. The equity value of a company depends therefore on the volatility of the market value of the company assets: the higher the volatility, the higher the value of the call. On the flip side, the higher the volatility, the higher the risk-neutral probability of default of a company liabilities - liabilities do not get to share the upside.

With each underlying (tradable) token locked in a vault characterised by a liquidation ratio, the value of the collateral could be estimated, in line with Merton, as the residual value of the assets (market value of the locked tokens) minus the value of a call option written on those assets with strike price equal to the liquidation ratio. As a consequence, a Merton approach can be used to estimate the appropriate stability fee and risk-weighting to assign, dynamically, to each collateral vault.

A more granular structuring of the collateral vaults along the risk spectrum (among tokens and for each single token), and a more robust estimate of the net exposures, could result in a very different calculation of protocol leverage. My intuition is that the value of DeFi’s net exposure is currently grossly overestimated.

A Potential Solution to the Pro-Cyclicality Problem

The idea of creating more granular, and dynamic, collateral vaults could also significantly mitigate the notorious pro-cyclicality problem of protocols like Maker1.

For collateral exposures like ETH, Maker currently offers different vault options:

ETH-B: 130% minimum collateral ratio, 9.0% stability fee

ETH-A: 150% minimum collateral ratio, 3.5% stability fee

ETH-C: 175% minimum collateral ratio, 1.0% stability fee

Those options allow the borrowers to choose which vault to use based on market conditions and their risk appetite: higher collateralisation/ lower leverage -> lower liquidation risk/ lower fees. But offering more pricing points only partially mitigates the pro-cyclicality issues.

What if instead those buckets were used in the same way banks categorise dynamically their loan book (in stages using IFRS9 jargon)? If, for example, the vault used by a borrower would fall below its minimum collateral ratio, rather than being immediately liquidated the exposure could move automatically to another, riskier, vault, characterised by a lower collateral ratio and higher fees. Liquidation would become the last available option in the same way credit collection is the last available option for a non-performing loan. This would:

Reduce the binary risk of liquidation for the borrowers, hence favouring use of leverage and DAI minting in asset deflationary phases

Optimise Maker profitability at different risk levels

Allow a more granular credit risk management

It might be worth discussing this with MakerDAO’s community.

Finding the Right Measure of Leverage

Traditional banks’ leverage ratio tries to account for a bank’s global unadjusted exposures, to credit and other types of commitments, both on-balance and off-balance. It is the most comprehensive measure of financial leverage available.

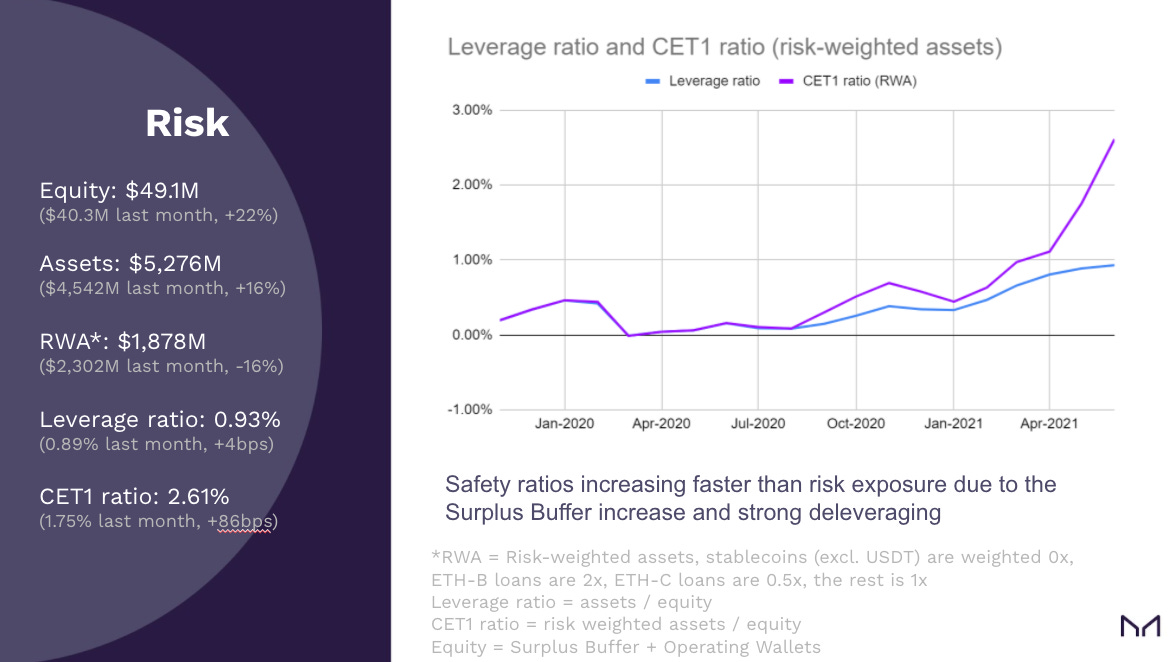

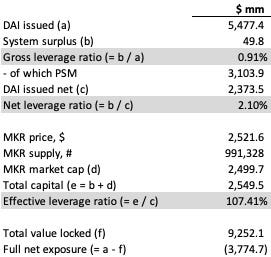

How does the 7.4% (or 8.4% if we focus solely on on-balance exposure) leverage ratio of BNP Paribas compare to Maker’s? Below are the numbers I calculated at the time of writing this post - DeFi banks have the benefit of real-time analytics.

Maker’s net leverage ratio (excluding stablecoin cash exposure) was 2.1%, significantly below BNP Paribas. However, as I mentioned before, I argue that MKR market capitalisation should be taken into account when calculating DeFi leverage; if we do it in full the effective leverage ratio of the protocol would be at 107.4%. But even if we decide to give <1 weighting to the MKR token capital backing the surplus - and we have all the arguments to do so, it doesn't take much to do better than BNP’s 8.4%.

In addition, Maker’s net exposure (net of locked value) is negative by 3.8b - the bank is effectively underlevered having more value locked than DAI minted. Obviously this is a very narrow perspective, because the market value of the underlying tokens is itself factoring in huge future value expectations. But the point still remains: if we consider even partially the value of the collateral in the leverage calculation - which we are not doing in the gross leverage ratio, Maker is significantly less levered than traditional banks. Without a central bank acting as a backstop with taxpayer’s money, it is a necessary evil: DeFi banking is simply a more comprehensive representation of the lending value chain.

Concluding Remarks

The paradigmatic changes brought in by the tokenisation of lending protocols are running much deeper than what immediately evident. The concepts of solvency capital, exposure, leverage, profitability, have been given a completely new meaning by the transparency and enforceability of smart contracts, in the same way the relevance of equity capital for an investor was transformed by the rise of stock exchanges.

We already live in a world with distributed risks and rewards. The difference is that in the world we are used to, central authorities act as bottlenecks in dealing with the distribution of those risks and rewards. This has had an impact on how we look at banks, among other things. With the ability of blockchain technologies of embedding directly in the banking infrastructure this distribution of risks and rewards, our ability to judge the quality of banking businesses and to assign them a value should become more comprehensive. The narrow definition of capital we are used to in traditional banking, for example, is inapplicable to DeFi banks, as we argued above.

A new risk management and valuation framework is therefore required, and although it is not the intention of this post that of being conclusive in suggesting one, I hope it will help sparking the conversations for the years to come.

Technical note on pro-cyclicality: Maker’s collateral pool is constituted by crypto-tokens that (currently) have a very high degree of correlation. As a result, users of the protocol are overall incentivised to mint DAI via posting collateral in asset inflationary phases (i.e. when they expect the price of the collateral to go up). On the contrary, during asset deflationary phases those users are incentivised to get back control of the collateral to avoid the risk of punitive liquidation, thus reducing the amount of DAI in the market - with additional impact on the peg. The introduction of full-reserve stablecoins such as USDC in the collateral pool and of a depositary rate mechanism has reduced this effect on the DAI, although still reducing the yield of Maker’s balance sheet during deflationary phases. During bear markets Maker resembles more a cash depositary institution than a lending bank. However, with the DAI acting as a small crypto overlay over bankcoin, the monetary transmission mechanism isn’t affected. However, in a fully blockchain-based economy where the monetary expansion function would be delegated only to banks like Maker, its pro-cyclicality would certainly become an issue.