# 7 | Is Asset Management Ready to Depart 1984?

Composer: Sweet Bitter Symphony

This is another issue of Dirt Roads. Those are not recaps of the most recent news, nor investment advice, just deep reflections on the important stuff happening at the back end of banking. Because banking is nothing but a pragmatic translation of our ability to imagine what hasn’t yet happened, but could. The time you dedicate to read, think, and share, is precious to me, I won’t make abuse of it.

Unification of Thoughts

Note. This week’s entry is largely about asset allocation and asset management in general, which isn’t usually a topic at the core of Dirt Roads. The post will intentionally avoid the discussion of ephemeral concepts like returns, benchmarking, alpha, modern or ancient portfolio theory, etc. In addition, the post will avoid dropping around names of celebrated investors like Buffet, Druckenmiller, Soros, and Swensen.

The asset management profession is a generous yet jealous mother, a mother with allaccepting love. On the one hand, it has been the perfect experimental space for mathematicians trying to code interactions among agents, both conscious (in the form of games) and unconscious (at least explicitly, in the form of uncertainty). On the other, it is the favourite domicile of information asymmetries, entrenched interests, artificial inefficiencies, and rent seeking. There is a lot in between. Nonetheless, all investors and allocators (i.e. the investors’ investors), from the angel warriors to the sleek gatekeepers, are trying to protect their position by making their area of expertise difficult to access or to comprehend. It is understandable, there is a lot of money at stake, so nobody has a real incentive to make it easier for money to find a home at the beginning (or the end) of the food chain.

There has been a lot of interest recently on how retail investors trade, and on what are the business models of the companies serving those traders. A lot has been written about the listing of Robinhood, and how the company innovated by transforming the traditional clients of brokerage companies (the retail investors) into the product to be sold to another group of clients (the institutional market makers). There are also other companies, like Alpaca, that are building a platform for those non-institutional traders to operate like professionals, offering the possibility to use code to program the trade flow. “We are all investors” says Robinhood, but we have always been investors I argue. Common savers are simply swapping one intermediary (a bank, a pension fund, an investment product provider) for another. Robinhood’s success is more a story of good marketing rather than structural or conceptual innovation - which is what we, in this newsletter, are ultimately interested in.

The food chain is just reshuffling. But for many, who live in the in-between, life is still pretty good.

Seven Little Bridges

Dirt Roads maintains a keen interest in the representation of knowledge. As I discussed in last week’s post on Superfluid, there is an intricate connection between the representation (and manipulation) of knowledge and that of financial value.

It is more than fair to say that asset management has gone a long way in abstracting basic concepts such as value, time, and uncertainty, so long that most investors ignore what are the underlying sources of the returns they are enjoying - at the various aggregation levels represented by contracts, securities, funds, funds-of-funds, pensions. The way we manipulate, package, and observe those investment primitives, however, still requires a lot of work. Part of the base layer - i.e. tradable liquid securities, has been hit by mathematics and computer science long ago. What happens at higher levels of abstraction, however, is still the kingdom of paper and Excel spreadsheets. Sure, there is a lot to improve, but how many have the incentives to do it? And how many can understand code anyway?

A Short Story of the Graphic Interface

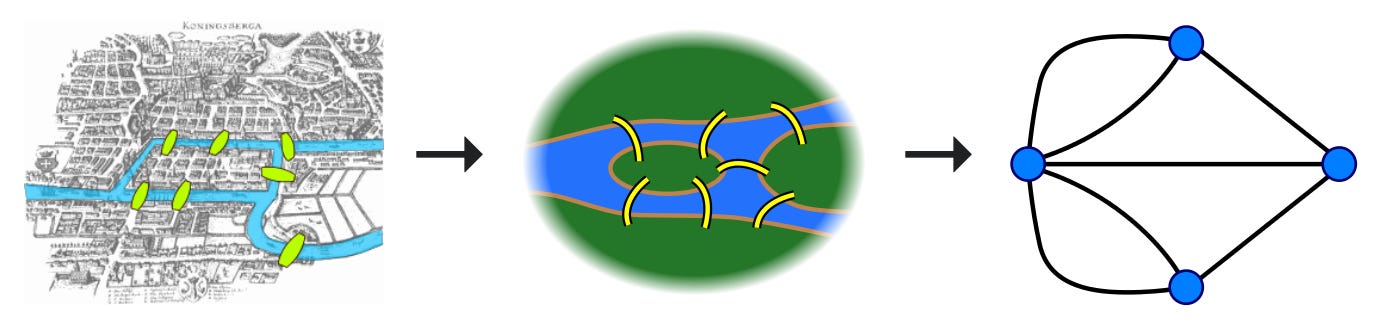

18th-century Königsberg had seven bridges connecting both sides of the Pregel River and the islands of Kneiphof and Lomse. The problem that the mathematician Leonhard Euler proposed to solve was the following: can you devise a walk through the city that would cross each bridge only once? In 1736 Euler proved that the problem has no solution, but rather than approaching the proof via the use of mathematical equations, he did it through graphical representation1. Graph theory was born.

The power of graph theory, since then adopted from physics to linguistics, lied in the ability to leverage the innate human ability to structure and absorb knowledge visually, rather than symbolically - equations came very late in the history of human evolution.

But it has been in computer science that our innate ability to think graphically has found its most powerful application - so far. Most of the early research in graphical user interfaces (GUIs) was based on the observation that children learn via primitives like eye-hand coordination rather than through the use of command languages. In 1973 Xerox developed Alto, the first personal computer using a desktop metaphor and a GUI. Legend says that Steve Jobs traded $1m in stock options to Xerox for a tour of their facilities and projects, and that Alto was the inspiration for Apple’s Lisa, the first GUI-based computer available to the public. Then, in 1984, Apple released the Macintosh, projecting it in worldwide culture with probably the most famous Super Bowl commercial ever. We have gone a long way since then, today almost everybody uses computers to perform sophisticated tasks of knowledge management and manipulation without any understanding of what happens behind the coloured screen.

The Composer Manifesto

So why has instead the experience of investing and managing assets barely changed during the last decades? Why investing softwares and interfaces haven’t caught up with the innovations in human-to-machine communication? In his wonderfully written Composer Manifesto Benjamin Rollert, CEO and co-founder, blames it to the excessive pragmatism of fintech (emphasis is mine):

“Why hasn’t software changed everything already? There’s likely no single, all-encompassing answer. But a likely culprit is that, to date, fintech software attempts have been too practical, lacking the boldness and radical product thinking we’ve seen in other domains. Instead of radical reform, they’ve focused on incremental change, automating a single step of a process here or removing a layer of friction there. Bolder action is needed. To break out of the current stasis, the entire infrastructure — human and machine — that underpins asset management needs to be rethought and rebuilt, starting with a blank slate.”

So what is Composer? Today, Composer is a (beta-versioned) graphic interface that supports investors in logically constructing, testing and automating their trading strategies, without the need to use code. This would be ambitious enough, but Rollert recognises, and I tend to agree with him, that the potential of semantically separating information gathering, trade execution, and idea generation, is way higher. Those three aspects, each important, of asset management, are currently mixed all together by monolithic providers of investment solutions. The Great Decoupling, as Rollert calls it, means separating those aspects and making the creation of investment strategies - or symphonies:

Interoperable, i.e. able to be plugged into any data or execution provider(s) - developing an investment strategy should be detached from sourcing high-quality data or dealing with the efficient execution of trades

Modular and extensible, for example to different primitives (e.g. new asset classes like crypto tokens, illiquid investments, etc.) or new concepts (e.g. new metrics, decision boundaries, dynamic logics, etc.) that belong to the investment decision making process

Shareable and communicable with others, being them clients, peers, reviewers, or authorities - you could purchase, or subscribe, for a symphony without buying the whole package that includes data management or trade execution and reporting

Immutable and versioned in the same way code and software applications are - for a rigorous post mortem analysis, risk management, backtesting, etc.

Monetisable, in a way that is more transparent than the current offering

How Composer Works

I put my name down to be a beta tester of Composer first iteration and got the call last Monday. It was a kind, personal, yet short one, because most of Composer’s features are still under development and a beta testing is the best way to get a sense of how it feels to compose a symphony.

There are a few pre-constructed symphonies on Composer when I log in. The one below is called NASDAQ Mean Reversion, and is constructed to capitalise on the performance dips of the index.

Reading what the strategy aims at doing is easy by following the tree. The logic checks for a few hierarchical conditions (in blue), and acts based on those conditions via identified weights (green) and assets (white). The rationale is clear: if there has been a recent dip in performance, and the index is not coming out of the dip, then the full weight of the symphony is assigned to a levered version of the index - betting on mean reversion; otherwise, the full weight is assigned to a safe short-term bond index ETF. The frequency of the conditions checking and rebalancing can be tuned, from daily to yearly, and the symphony can be backtested and benchmarked (ok, I used the b word).

The allocation chart below shows when the symphony went “risk on!” - in yellow; there are very few days when both conditions were satisfied and the symphony put money at work, still it was able to generate significant returns (ok, I use the r word).

In addition to backtesting the company already provides, through Alpaca, the ability to live or paper trade for US-based investors, but that wasn’t available for me.

Although still way in its infancy and so far targeted more to the recreational-plus-plus trader than the pro, Composer offers already several possibilities to create symphonies through conditions, filters, weights, and assets to invest in - both statically and dynamically. It doesn’t take much to unlock creativity and start thinking of infinite permutations to upgrade symphonies, and I believe that to be the ultimate intention of the software. The Slack group of beta testers I am part of is already full of ideas, shared symphonies, requests for additional data or assets to invest in - the question is how and when will Composer be able to incorporate those interactions without screwing the user experience.

The true composability and flexibility of the interface will indeed be THE challenge - with the myriad of data providers and execution platforms, will the platform be flexible enough to offer a high-quality experience to its users while expanding its potential - endogenously or through APIs? Composer has big ambitions and hard work ahead, as well as the well known difficulty of ensuring engagement and transforming this engagement into a revenue stream. The combination of subscriptions and revenue share from users’ monetisation could be viable, but a lot needs to be tested and this post is in no way a company SWOT analysis or valuation. We must confess that most of the profitable companies active in asset management are still doing money at the expense of somebody else rather than by being value accretive. However, I read once that if you are pitching your early-stage idea to an investor and the investor asks you for your views on the path to profitability, you are pitching to the wrong investor, so I don’t want to make the same mistake.

For completeness, the company closed a seed round a couple of months ago.

East Coast vs. West Coast

I was attracted by Composer for two distinct reasons: (1) their intention to kick-off the adoption of GUIs in asset, or more generally, value management, and (2) the implied effect of separating semantically the creative moment from other activities. Sure, there is a lot of creativity involved in engineering data or synthesising information in reporting, but separating those moments would benefit the whole process and enhance trust as a consequence.

Both are bold ambitions that might have a huge impact on the industry, but both will depend on innovations happening at the back end. The landscape of data providers and access channels for investing is messy, patchy, and often anchored on very old tech (namely, paper). It is also crowded, heavily regulated, and much lobbied for. It is not a case that most of the innovations in the Web 2.0 era happened in the free-for-all Far West of personal data use.

Synergies with blockchain technologies are evident. The tokenisation of data and value would turbo-boost modularity and, on the other hand, UX remains one of the weakest aspects of the crypto economy. Composer is trying to solve the conundrum starting from the Old World, which still intermediates the vast majority of financial value, while others are trying to do the same in the New although with a way less ambitious approach. Time will determine who will be the winner when the Great Convergence comes.

From Wiki: “In modern language, Euler shows that the possibility of a walk through a graph, traversing each edge exactly once, depends on the degrees of the nodes. The degree of a node is the number of edges touching it. Euler's argument shows that a necessary condition for the walk of the desired form is that the graph be connected and have exactly zero or two nodes of odd degree. This condition turns out also to be sufficient—a result stated by Euler and later proved by Carl Hierholzer. Such a walk is now called an Eulerian path or Euler walk in his honor. Further, if there are nodes of odd degree, then any Eulerian path will start at one of them and end at the other. Since the graph corresponding to historical Königsberg has four nodes of odd degree, it cannot have an Eulerian path.”