# 51 | Communicating Vessels: Escaping Liquidity‘s Catch-22s

Aqueducts, Interest Rates, Ondo Finance, and the Old But Gold Risk Free Rate

I have inherited quite a few things from my mother. The abrasive yet heavily relied upon get-shit-done mindset, the urgency to speak unnecessary truths in socially sensitive environments, the demonic pleasure to put salt on somebody else’s obvious flaws—as well as my own, and the passion for Piranesi’s etchings of ancient Roman views. During the 18th century Giovanni Battista Piranesi, artist and archeologist, produced a long list of those, gaining a lot of attention across the Europe of the Grand Tour. Among the images of prisons, churches, and squares, were those of ancient aqueducts, once upon a time testament of Rome’s ingenuity and political dominance. Everything, since the days of Piranesi, had changed around those structures made of brick, stones, and mud. Everything but the structures themselves, pieces of history I could still visit—and I did, stuck in their decrepit state. They were everywhere, dispersed throughout the city behind traffic lights and trash bins, immune to the insignificance of us all, an infinite succession of arches that had carried for centuries water (hence life) from the centre of the Empire to the periphery of mankind, and that now laid abandoned and ignored.

| Леди справедливость, Векторная иллюстрация, Иллюстрации")

Interest Rates and the Global Value Level

It is just wealth for its own sake. We heard it before. Ancient age aristocrats, medieval money lenders, Wall Street bankers from the eighties, 2001 dotcom newly-found entrepreneurs, 2007 financial engineers, 2020 crypto gurus. And the list will go on. And the confusion will remain. Why should those folks get rich so quickly and so incredibly? What are they doing exactly for society? What’s the product of their actions? Is what they are doing real innovation? It is an eternal fight: on one one side the conservatives—those who perfected the understanding of the recent past, on the other the innovators—those possessed by the desire of shaking off local optima, and in the middle the speculators—those praying on the always-swinging pendulum that oscillates between unstoppable optimism and hyper-informed pragmatism. It’s the innate fight of the humans against the slope of spacetime.

The twenties (as in the 2020s) haven’t been different. Today’s financial pipes work, it is undeniable; they connect the whole world at quasi-instantaneous speed and allow the transmission of value (liquidity) and information (pricing) from central banks all the way to the ultimate beneficial borrowers. It is also undeniable, however, that today’s financial pipes suck—try to step into the compliance department of a bank. But what should be preserved and what should be sacrificed? The resilience guaranteed by what’s known or the efficiency promised by what is yet to come? And so the conservatives—those who are already rich, and the innovators—those who want to get rich, debate. In the meanwhile, the world keeps changing.

Rome Is Pumping

Main-stream → It is the 25th of March 2020, and the pandemic is raging. Daily US Treasury par month rates hit 0.0%: the economy needs help and the Fed (and its peers) is (are) delivering. Everything is connected, and so the intensified flows of liquidity reach every corner of the risk spectrum, lowering benchmarks and increasing pricing for all risk classes. Translation: the price of everything goes up. Of everything that doesn’t move, actually—i.e. everything governments do not measure inflation on. The whole world, let’s not forget, is locked at home. Nasdaq, a proxy of the global appetite for far-away profits, is climbing and will keep climbing for a while, reaching its ATH on the 22nd of November 2021 at intraday 16,212.23.

Alt-stream → Liquidity along the Fed’s aquaeductus, however, is reaching alert levels, and music can’t be stopped so easily. Not only future yield, but also current prices, depend on it—extraordinary returns are indeed addictive. And so central bankers decide to close their eyes, allowing the liquidity to keep flowing. This is not the whole story, however. While the financial main-stream was busy channeling liquidity along proven rails, groups of self-organised builders were heads-down developing an alternative system to transmit water across the land. The motives behind that push were multiple. The new pipes aren’t ready, it’s still a fun zone for the avant-garde. Yet, it doesn’t matter: pressure is too high and water needs to go somewhere. And so someone decides to plug the two systems, the old and the new, and help water flow naturally from one container to the other.

In March 2020 the total floating amount of US-backed1 stablecoin was few billions. That number would reach c. $160b at ATH. Stablecoin outstanding float is definitely an imperfect measure of the amount of liquidity that flows on crypto-rails, but one that is good enough to assess direction and magnitude of liquidity shifts, and also one that leaves less space to debate. The (truly) winning businesses in this environment were, not surprisingly, the bridge operators: Circle, and Tether, above everyone. In the process the tide lifted everything else, what made sense and what didn’t.

Rome Ain’t Pumping Anymore

At some point, however, the music had to stop. And it did. As abruptly as it had started. By Q3 2022 US par month rates exceed 1.0%, then 2.0%, then 3.0%, then 4.0% before the year ends—they currently sit at >4.5%. Central banks are pulling the plug fiercely and disorderly. Everything starts crumbling, and it is not for me to tell that story again. Something else, however, happens: the wall of money that had moved from one system to the other, from the old to the immature new, doesn’t flow back as rapidly as expected, and not as rapidly as the downward movement of (digital) asset prices—that are arguably a nimbler representation of crossover expectations. By the end of 2022 US-backed stablecoins stabilise around $130b with Tether’s $USDT—c. $65b, Circle’s $USDC—c. $45b, and Binance’s $BUSD—c. $15b, as the clear winners. The motives behind the inertia are hard to tell but fact remains that while on traditional rails money yields >4.5% per year to just do nothing, the like-for-like return for cash on the alternative system is at best 100 bps. The difference in pressure is massive again as in early 2020, just in opposite direction. It is a new microclimate, a perfect one for the emergence of another generation of bridges.

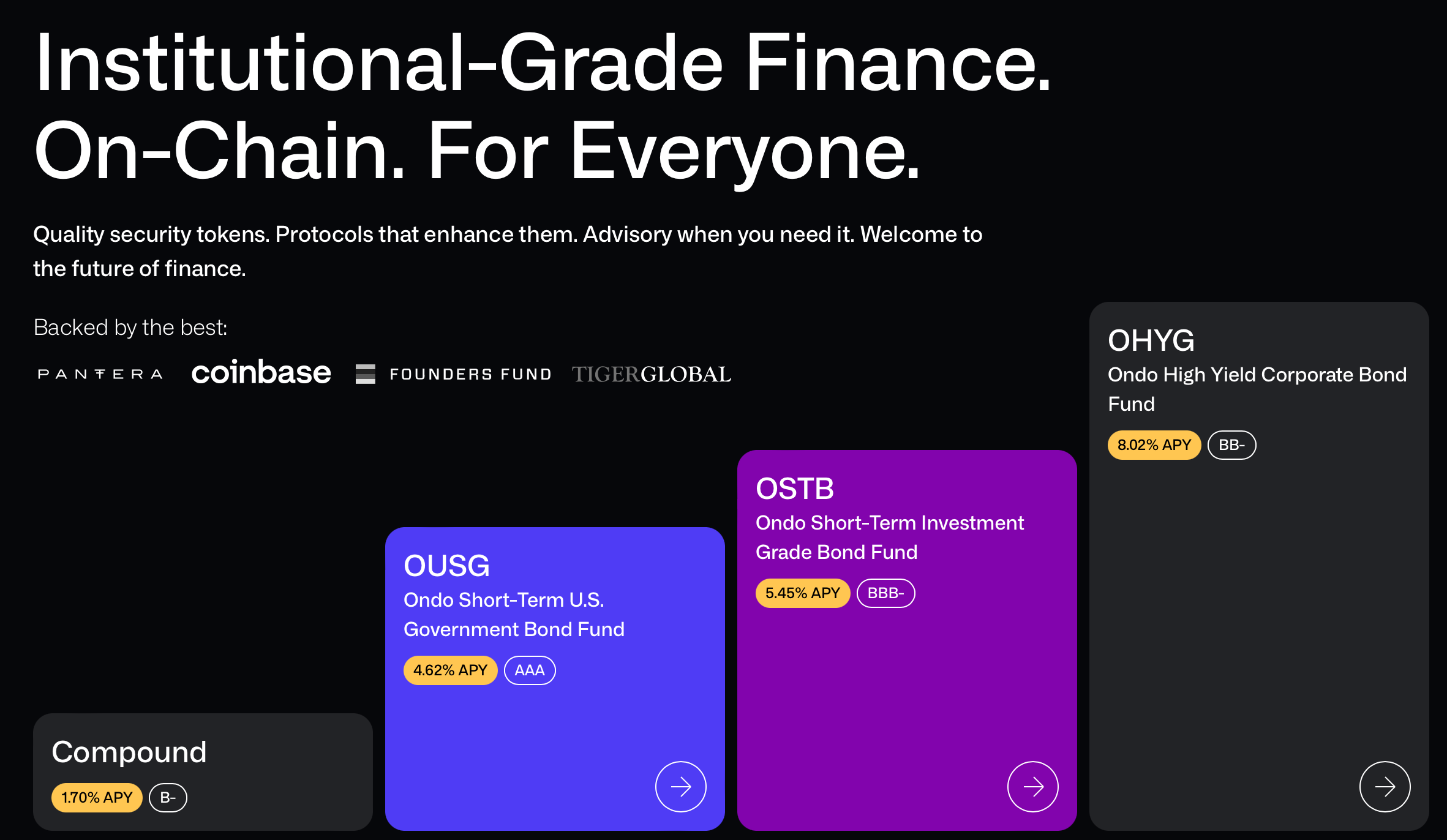

Ondo → Teams in the DeFi sphere haven’t been watching without doing anything while their legacy business evaporated and, at the beginning of 2023, Ondo opened the dances. Early into January the protocol announced on Twitter the ability for holders of crypto and non-crypto liquidity to invest directly through the platform on a set of yield-bearing opportunities—with the yield this time generated in the real rather than digital world. The platform would allow qualified users to subscribe to strategies deploying liquidity on US Government Bonds—$OUSG, Short-Term Investment Grade Bonds—$OSTB, and High-Yield Corporate Bond—$HYG. It was a radical pivot for the project, originally offering on-chain structured finance solution to DAX liquidity providers, but one informed by the huge market opportunity. With the launch of its v2, that came paired with a dedicated Compound fork called Flux, Ondo would allow yield from the real-world to access DeFi’s trapped liquidity and start deploying battle-tested frameworks (like Compound’s decentralised money-market) on top. The classic plethora of enthusiastic Twitter proclaims didn’t have to wait long.

For as much as Ondo’s pivot has been a welcome step towards the bi-univocal integration of the two systems, the devil remains in the detail—and there’s a lot of detail to digest. Unfortunately, looking under the hood things get less exciting than on Twitter.

Structuring → Rather than developing new financial packages Ondo’s v2 builds on what already exists out there—and for good reasons, in this case on BlackRock’s iShares ETFs. That means that purchasing Ondo’s $OUSG means investing through a crypto-friendly front-end into a Ondo-managed fund that invests into another BlackRock-managed traded fund that invests into government-issued ETFs. Fees add up.

Access → Rather than being permissionless, investing in Ondo’s v2 (i.e. purchasing Ondo’s $O*** tokens) is subject to customary KYC and to successful classification as qualified purchaser, i.e. as an investor (private or institutional) that deploys at least a few millions in liquid securities. An anonymous wallet address cannot interact with $OUSG’s minting engine nor exchange $OUSG freely in the open market.

Composability → It is unclear how transmissible will those units be across the DeFi ecosystem, and it is not a minor detail. The automated market-making construct pioneered by Compound, for example, is built upon the ability to liquidiate the non-performing assets provided as collateral by borrowers. Unfortunately the same concept cannot be applied as easily in a permissioned setting. Below, an extract from Flux’s documentation—emphasis is mine. We can summarise what’s written in the docs as follows: liquidations don’t work in a permissioned environment, but as long as the collateral has limited credit risk (and limited duration risk at the current interest rate levels) it won’t matter. This isn’t great for composability, and financial systems are all about composability.

Liquidations on Flux are very similar to liquidations on Compound V2.

An account becomes subject to liquidation when its liquidity (i.e. the aggregate collateral factor of its assets) becomes negative. At that point, a third-party liquidator will be able to pay off some of the borrower's debt and seize the corresponding collateral at a small discount. The protocol will also collect a small piece of the collateral and add it to its reserves.

However, unlike on Compound, liquidations on Flux respect the underlying asset's permissions (e.g. KYC). For example, to liquidate an account using OUSG as collateral, the liquidator must be KYC'd and whitelisted to hold that token.

[…]

The protocol aims to ensure every account always has positive equity. However, in scenarios of extreme volatility, an account's equity might become negative when the LTV increases too quickly before it can be liquidated. In such cases, the borrower and liquidators are not incentivized to pay back the debt, so the protocol and its lenders accrue bad debt (losses).

Bad debt accrual should be extremely unlikely on Flux since its assets are generally very stable. As an additional safety mechanism, Flux's stablecoins oracles never price them at more than 1 USDC, reducing the risk of external oracle manipulation.

Escaping perennial judgement → What Ondo’s team is doing is nevertheless great for signalling. Ondo is not alone in trying to reconnect the two worlds and get a cut in the process. Maker has been trying to deploy money (this time minted permissionlessly) back into government paper for a while and has now $500m at stake—arguably the most relevant hybrid experiment in crypto so far, Backed has been working on an alternative construct to tokenise real assets—what that will mean we don’t know yet, Credix has started to work in sync with stablecoin issuers to provide collateral backing for the minting. The opportunity is clear and many others will come.

Notwithstanding all this, it won’t be enough. Rather than focusing on patching the old system and the new at the whims of macroeconomic flows, we should keep working on innovating the rails that move value around. Rather than building layers on top of layers to expand market reach for the benefit of the same products we were originally trying to dethrone, we should aim at demolishing and recomposing them differently. Rather than being timidly afraid to challenge the wisdom of regulators, we should courageously raise our head and guide the dialogue around compliance with expertise and ambition. The mission is huge but the prize enormous. We will need courage if we want to transform the highways of todays into the mere backdrop of historical dramas of tomorrow. Those who will provide the ability for institutional-grade collateral to be ported on-chain while at the same time preserving the permissionless and composable nature of decentralised financial blocks will make history, and get very rich.

Don’t quote me on the appropriateness of the word backing